As in Income Tax Notice Part-1, we discussed why notice is sent, the types of income tax notices are and how to verify the authenticity of an income tax notice and how to Income Tax Notice Response Online.

Now in Part-2 we focus on the most critical aspect - how to respond correctly to an income tax notice, penalties and consequences for ignoring the income tax notice and some special tips to avoid income tax notices.

How to Respond to an Income Tax Notice?

Steps to follow:

1. Read and understand the notice carefully

2. Verify the authenticity of the notice through the income tax portal

3. Now collect all the documents which are asked for, like Form 16, bank statements, investment proofs and other details

4. Draft your response with a clear explanation and documents collected and submit your response on the income tax portal

Most income tax notices must be responded to online through the Income Tax e-Filing Portal, unless the notice specifically allows offline submission.

5. Download the acknowledgement ID for further reference

6. Always track the portal for further communication with the income tax department

Note: Failure to submit a response within the prescribed timeline may result in ex-parte (best judgment) assessment, additional tax demand, interest and penalties.

Deadline for each Notice:

| Notice Type | Purpose | Deadline for response |

| Section 139(9) | Defective return | Within 15 days of Notice |

| Section 142(1) | Inquiry / Document required | As specified in the notice |

| Section 143(1) | Intimation | Usually within 30 days (Response required only if there is a demand or discrepancy) |

| Section 143(2) | Scrutiny | As per the hearing schedule |

| Section 148 | Income escaped / Reassessment | As specified in the notice |

| Section 156 | Tax demand | Payment required within 30 days, failing which interest @ 1% per month under section 220(2) is applicable. |

| Section 245 | Refund adjustment | Within 30 days of Notice |

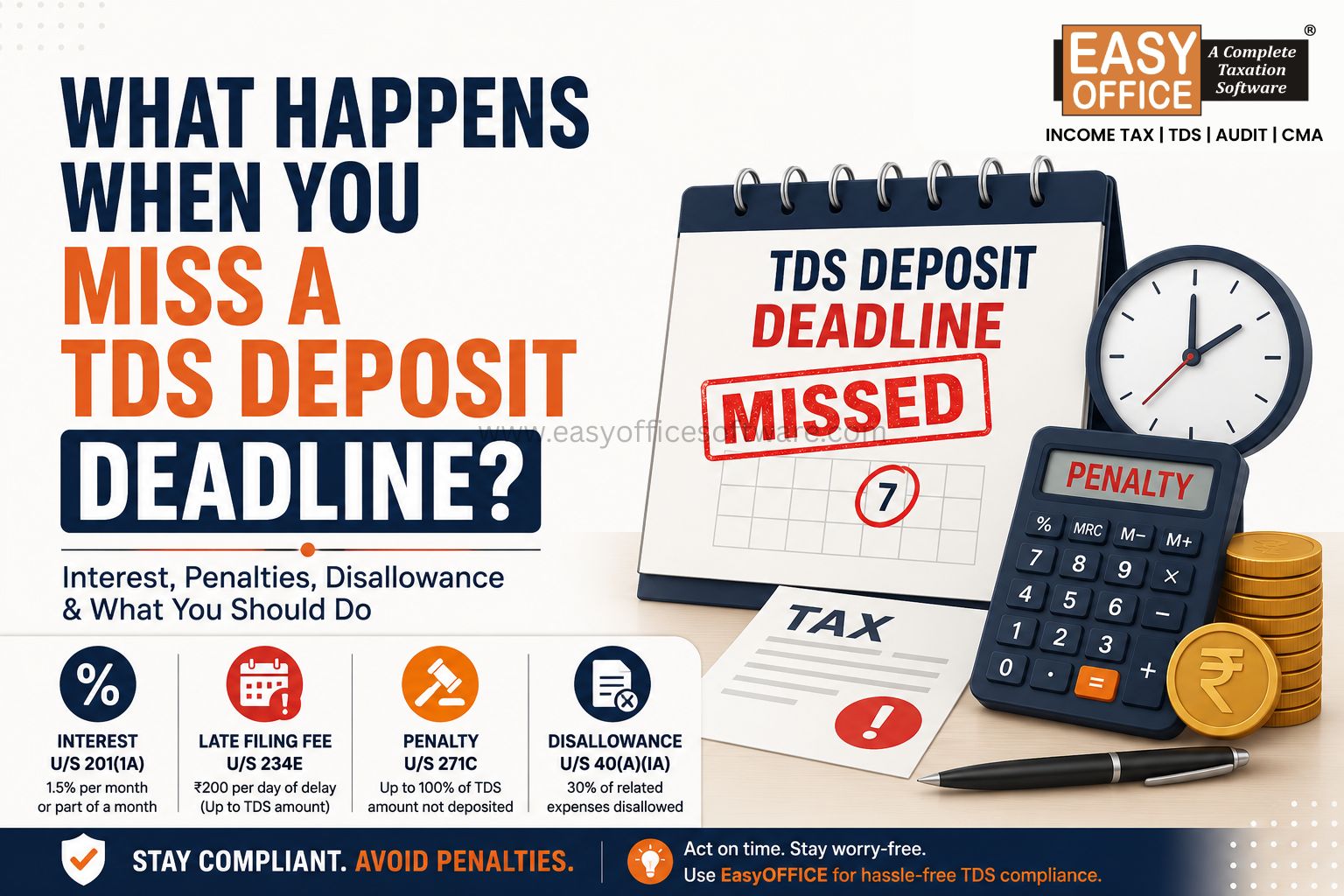

Penalties for Ignoring a Notice:

1. Notice under section 139(9) for Defective Return:

Failed to rectify the return within 15 days, ITD will consider the return as invalid, meaning loss of refunds, loss of carry-forward losses and possible late fees/interest.

2. Notice under section 142(1) for Inquiry before Assessment:

Non-compliance may attract a Penalty of ₹10,000 for each failure u/s 271(1)(b), may result in ‘best-judgement assessment’ (section 144) and prosecution

3. Notice under section 143(1) for Intimation:

Failed to respond to an intimation within 30 days, the tax officer passes notice with finalization of tax demand, followed by interest and recovery proceedings.

4. Notice under section 143(2) for Scrutiny Assessment:

Non-compliance allows the tax officer to proceed with “Best Judgment Assessment” (section144) or penalty of Rs. 10,000 for each failure to respond (section 272A)

5. Notice under section 156 for Demand Notice:

Interest under section 220(2) @1% per month is mandatory; recovery proceedings may follow.

6. Notice under section 245 for Adjustment of Refund against Demand:

If a timely response is not provided, then the refund will be automatically adjusted to pay for the outstanding liability identified in the notice

Tips to Avoid Income Tax Notice:

It is important for every taxpayer, tax professional and CA to make sure that income tax notice doesn’t arrive and for that tax payer should follow these practices:

> Filing ITR accurately and timely

> Reconcile income details with Form 26AS/AIS/TIS

> Disclose all income related to capital gain, freelance income and rental income

> Report high-value transactions correctly

> Do not claim unsubstantiated deductions

> Respond promptly to Section 143(1) intimations

Simplify Income Tax Notice Responses with EasyOFFICE

Handling income tax notices manually can be time-consuming and risky. EasyOFFICE Income Tax Software helps CAs and tax professionals:

> Track all income tax notices from a single E- Proceeding dashboard

> Upload, manage and link supporting documents easily

> Respond online within deadlines to avoid penalties

> Maintain a complete notice-wise compliance history

Related Blogs

All in one Software

- Income Tax Software

- TDS & TCS Software

- Audit e-filing Software

- CMA Data Software

Penalty for Late Filing of Income Tax Return for FY 2025-26 – Section 234F of Income Tax Act 1961

#ITR