Central Board of Direct Taxes (CBDT) has notified New Income tax Rule, 2026 which are applicable from 1st April 2026. This year is the Transition year from Income Tax Rules, 1962 to Income Tax Rules, 2026.

Understanding these changes is crucial for taxpayers to avoid errors in tax filing and to plan their taxes effectively under the revised rules.

In this Article, we will discuss about House Rent allowances (HRA), Salary allowance and compliance requirements. As CBDT has changed major 6 income tax rules that significantly impacts salaried taxpayer, including enhanced Exemption for Children education allowance, Hostel allowance, Meal Benefits and Gifts allowance. Taxpayers must exercise cautious while claiming exemption as the Income tax Rules 1962 has been replaced by Income Tax Rules, 2026.

Income Tax Allowances and Exemptions:

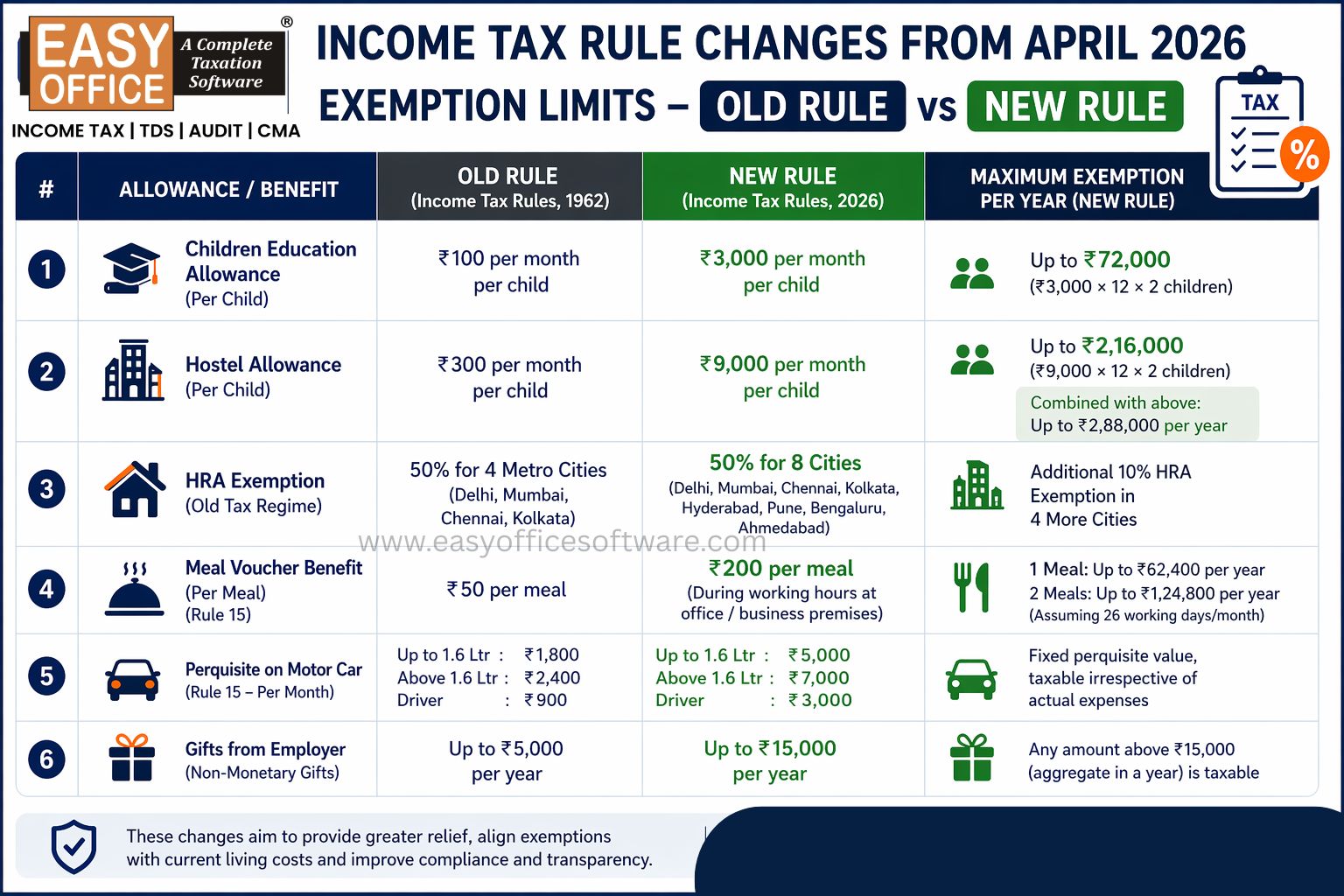

1. Exemption Increase in Children Education Allowance -

Under Income Tax Rules 2026 notified by CBDT, there is an increase in Children Education Allowance available for exemption to salaried taxpayer.

i. Earlier exemption: ₹100 per month per child

ii. Revised exemption: ₹3,000 per month per child

iii. Maximum children allowed: 2

This allows taxpayer to claim up to ₹72,000/year (₹3000 * 12* 2 children). This provides a major relief to salaried Individuals.

2. Increment In Hostel Allowance

Hostel allowance has increased under new rules.

i. Earlier exemption: ₹300 per month per child

ii. Revised exemption: ₹9,000 per month per child

iii. Maximum children allowed: 2

Allowing a maximum exemption of ₹2,16,000/year (₹ 9,000*12*2 children).

👉 If we combined Children Education Allowance and Hostel Allowance, this can go up to ₹ 2,88,000/year.

3. HRA rule going to more cities (Under Old Tax Regime)

3. HRA rule going to more cities (Under Old Tax Regime)

In past there were only 4 metro cities with exemption of 50 %. These were Delhi, Mumbai, Chennai and Kolkata. Now, we have more cities added – Hyderabad, Pune, Bengaluru and Ahmedabad. So previously we had 40% HRA in these metro cities but now Taxpayer can avail additional 10% HRA exemption, resulting in 50% HRA. So now there are total 8 cities.

4. Meal Voucher Benefit Increased

The non-cash meal benefit exemption has been enhanced under Rule 15 of the Income-tax Rules, 2026.

i. Earlier limit: ₹50 per meal

ii. Revised limit: ₹200 per meal

There are some conditions for this rule:

i. It must be provided during working hrs.

ii. They must provide it at Office or Business Location.

iii. It must not exceed ₹ 200.

If we assume that there is 26 working days in a month so

>> 1 meal per day - ₹5200/month and ₹62400/year.

>> 2 meal per day - ₹10400/month and ₹124800/year.

5. Perquisite on Motor Car (Rule 15 – Valuation of Perquisites)

The valuation of car perquisites for salaried employees is governed by Rule 15 of the Income Tax Rules, 2026. The taxable value depends on engine capacity, usage of the car, and driver facility.

| Particulars | Amount (New Rule) | Amount (Old Rule) |

| Engine Up to 1.6 litre | ₹ 5000/month | ₹ 1800/month |

| Engine Above 1.6 litre | ₹ 7000/month | ₹ 2400/month |

| Driver (additional) | ₹ 3000/month | ₹ 900/month |

💡 These values are fixed perquisite amounts and are taxable irrespective of actual expenses incurred by the employer.

6. Gifts from employer

The exemption limit for non-monetary gifts from employers has been increased:

i. Earlier limit: ₹5,000 per year

ii. Revised limit: ₹15,000 per year

Any aggregate value exceeding ₹15,000 in a financial year will be taxable in the hands of the employee.

Conclusion

The Income Tax Rules, 2026 introduce greater transparency and practicality into Indian taxation system. With enhanced exemption on Children Educational Allowance, Hostel Allowance, Meal Benefits and Wider HRA Coverage with adding 4 more cities, the revised rules better align tax benefits with current living costs.

In this evolving tax environment, taxpayers must stay informed, structured, and compliant while planning their finances effectively.

Income Tax Rules 2026 : Allowance exemption to Salaried employees

Related Blogs

All in one Software

- Income Tax Software

- TDS & TCS Software

- Audit e-filing Software

- CMA Data Software

Penalty for Late Filing of Income Tax Return for FY 2025-26 – Section 234F of Income Tax Act 1961

#ITR