Late Filing consequences are often the first thing taxpayers realise only after the due date has passed. The income tax return filing deadline for FY 2025-26 will result in financial penalties, benefit losses, and create additional compliance challenges for taxpayers who fail to meet it. The Income Tax Act, 1961 introduced Section 234F to discourage delays and to ensure timely filing across all taxpayer categories.

The blog explains how Section 234F works, who it applies to, and the penalty that is charged. With the right information, taxpayers can stay compliant without last-minute panic.

What is Section 234F?

The Income Tax Act, 1961 Section 234F requires taxpayers to pay a specific late filing fee when they submit their income tax return after the provided deadline. Section 234F functions independently of tax obligations, while interest provisions are calculated based on the amount of tax owed. The intent is simple. Mandatory filing requires all taxpayers to submit their returns on time.

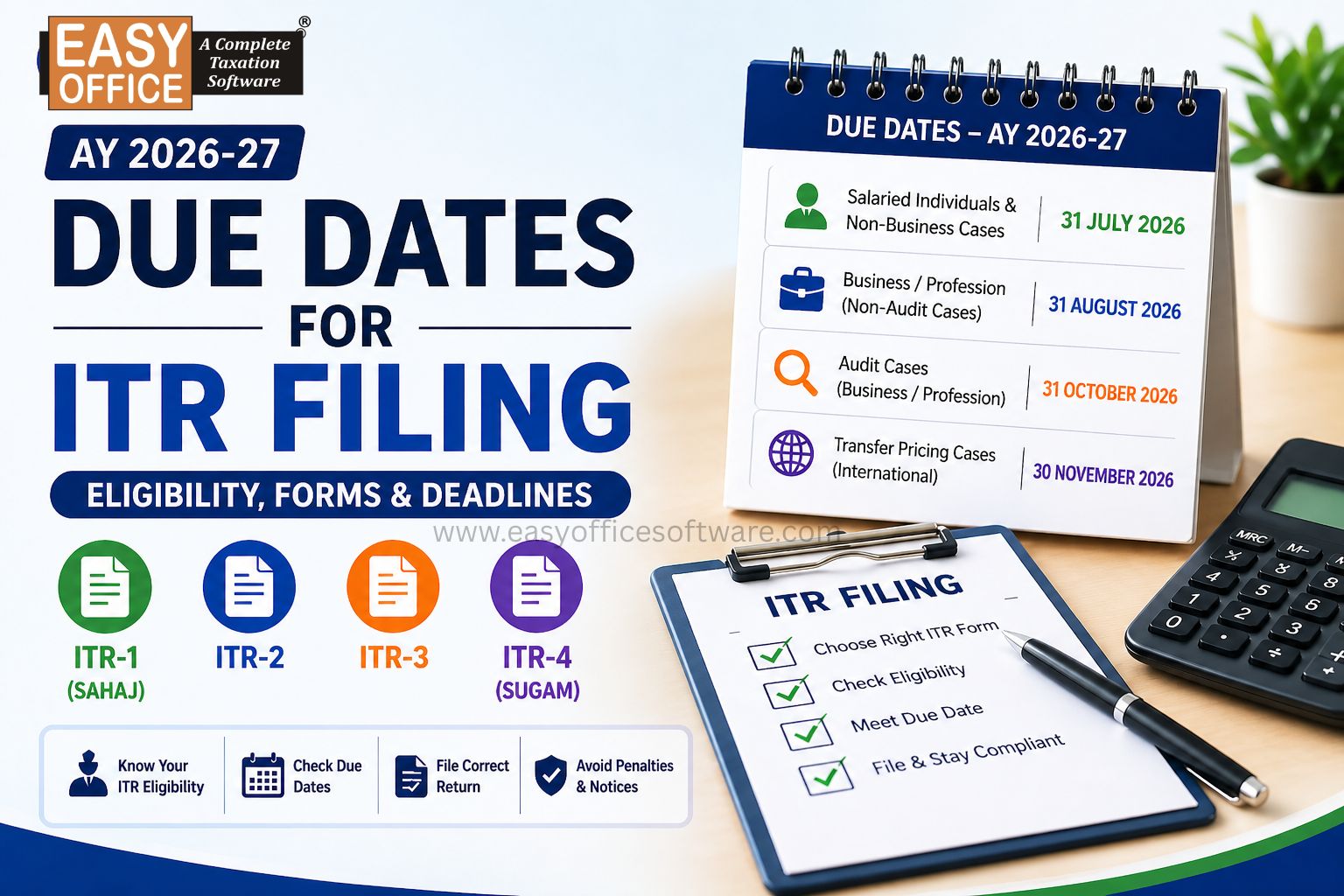

For FY 2025–26 (AY 2026-27), the standard due date for individuals Non Business cases (ITR 1 and ITR 2) is expected to be 31st July 2026 and for Individual Non Audit Business Cases its 31st August 2026. The Due Date is expected to be 31st October 2026 for the audit case. But, filing after this date automatically attracts a penalty under Section 234F.

This provision applies to individuals, Hindu Undivided Families, firms, LLPs, companies and other assessee that are required to file a return under Section 139(1).

Penalty Structure under Section 234F (FY 2025-26)

The fine is computed based on two Factors

The Due date of filing and the Annual Taxable income of the taxpayer.

Late filing fee table for FY 2025-26

| Annual Taxable Income | Late Filing Fees u/s 234F |

|---|---|

| Up to ₹5 lakh | ₹ 1,000 |

| Above ₹5 lakh | ₹ 5,000 |

The income tax portal automatically calculates this fee during the filing process. There is no discretion involved. Once triggered, it must be paid before the return can be successfully submitted.

Who must pay the Section 234F penalty (Applicability)

Section 234F applies to taxpayers who are mandatorily required to file an Income Tax Return under Section 139(1) but fail to do so within the prescribed due date. The penalty is imposed because the taxpayer failed to submit their ITR on time, irrespective of tax obligations and refund status.

Section 234F Is Applicable To:

• Individuals whose total income exceeds the basic exemption limit

• Hindu Undivided Families (HUFs) required to file returns

• Firms and Limited Liability Partnerships (LLPs)

• Companies, including private and public limited companies

• Freelancers and professionals with taxable income

• Taxpayers eligible for refunds but filing after the due date

The late filing fee applies even if:

> All taxes have already been paid through TDS

> No additional tax is payable

> The return is filed voluntarily

Section 234F Is NOT Applicable To:

• Taxpayers whose total income does not exceed the basic exemption limit

• Persons not required to file a return under the Income Tax Act

The fee under Section 234F becomes automatic and non-waivable after the due date under Section 139(1) has been missed.

Steps to Pay Section 234F Late Filing Penalty

The Section 234F penalty is to be paid through the Income Tax e-Filing Portal and is integrated into the return filing process.

Step-by-Step Process:

Step 1: Log in to the Income Tax Portal

The official income tax e-filing website requires you to enter your PAN and password to access the portal.

Step 2: Start Filing Your Income Tax Return

You need to select the assessment year that applies to your specific ITR form.

Step 3: System Auto-Calculates the Late Fee

The portal calculates the Section 234F penalty based on your total income when you file your return after the due date.

Step 4: Review Tax Payable

The late filing fee appears under “Fee and Interest”. Verify the amount before proceeding.

Step 5: Pay the Outstanding Amount

You can make the payment through online channels, including net banking, debit card, UPI, and other authorized payment methods.

Step 6: Submit the Return

The process of completing the return submission and e-verification begins after payment has been confirmed as successful.

The return process requires payment of the Section 234F penalty before you can proceed to file or verify your return.

Other consequences of late filing beyond the penalty

The Section 234F fee is only one part of the cost of late filing. Delays trigger several other disadvantages. The taxpayer loses the right to carry forward all types of losses, like capital and business losses. Refunds experience major delays.

Interest under Sections 234A and 234B may also apply if tax remains unpaid. Late filing increases the possibility of receiving greater scrutiny in certain situations. The total cost of late filing exceeds the penalty amount because of various financial effects.

If you fail to file your income tax return on the due date, you will be liable to pay interest at 1% per month or part of a month on the unpaid tax amount, as per Section 234A of the Income Tax Act. Your ITR wont be validated to file if the payment is due.

How to Avoid Late Filing Under Section 234F (FY 2025-26)

Section 234F penalties for late filings can be easily avoided. The official guidance documents present compliance issues that require taxpayers to implement these practical methods, explained clearly and without assumptions:

i. Start early with income consolidation

Salaried individuals should collect Form 16 early, while freelancers and professionals should track their invoices, bank credits, and expense records to succeed with their work.

ii. Reconcile Form 26AS, AIS, and TIS in advance.

Mismatches between Form 16, Form 26AS, and AIS are a major reason for delayed filing. The process of early reconciliation enables time to identify and fix their errors, and follow up with deductors.

iii. Estimate and plan the advance tax correctly

Freelancers and self-employed taxpayers often underestimate advance tax. Proper estimation helps taxpayers avoid payment problems that delay return filing.

iv. Avoid last-day filing risks.

Portal congestion, OTP failures, and validation errors are common near deadlines. Early filing protects you from technical issues that can push you past the due date.

v. Use income tax return software instead of manual tracking

The reliable income tax return software system can automatically input data from AIS and Form 26AS, flag missing income, and calculate tax accurately, reducing the need for manual verification.

vi. Enable automated reminders and dashboards.

Professional income tax return software sends deadline alerts and provides filing status visibility, which is essential for individuals, CAs, and tax professionals handling multiple returns.

vii. Ensure correct regime selection before filing.

Institutional tax declaration software matches both existing and upcoming tax systems to provide users with accurate comparison results.

Using income tax return software has become an essential tool. It is the most effective method to avoid Section 234F penalties and achieve precise compliance within required deadlines.

Conclusion

Section 234F has made timely filing non-negotiable. The fiscal year 2025-2026 (AY 2026-27) imposes penalties for delay, which creates avoidable penalties that serve no actual purpose. The smartest way to protect yourself from penalty for late ITR filing FY 2025-26 is to be prepared backed by automation.

EasyOFFICE Income Tax Return Filing Software is built for freelancers, Chartered Accountants, tax professionals, and businesses in India who want accuracy without anxiety. EasyOFFICE ensures your return will be submitted before the due dates. This income tax return software will remind you about your return, and it will be filed before penalties even become a thought.

FAQ

1. Is Section 234F applicable if I have a refund?

Yes. The late filing fee applies even if the return results in a refund or no Tax Liability.

2. Can the Section 234F penalty be waived?

No. Once the due date under Section 139(1) is missed, the fee becomes mandatory and system-generated.

3. Is Section 234F applicable if tax payable is zero?

Yes. The fee applies regardless of tax payable.

Section 234F, Late Filing Penalty, Income Tax Return India

Related Blogs

All in one Software

- Income Tax Software

- TDS & TCS Software

- Audit e-filing Software

- CMA Data Software

Penalty for Late Filing of Income Tax Return for FY 2025-26 – Section 234F of Income Tax Act 1961

#ITR