A newer tax regime has been proposed by the Finance Bill, 2020 for Individual and HUF to tax the income of such persons at lower tax rates from F.Y. 2020-21 (A.Y. 2021-22) and onwards, if they agree to forego prescribed deductions and exemptions and fulfill certain conditions as mentioned under the Income Tax Act (hereinafter referred as “Act”).

- Special provision for calculating income of person opting for this tax regime is prescribed under Section 115BAC of Act.

| Taxable Income | Rate of Income Tax |

|---|---|

| Up to Rs. 2,50,000 | Nil |

| From Rs. 2,50,001 to Rs. 5,00,000 | 5% |

| From Rs. 5,00,001 to Rs. 7,50,000 | 10% |

| From Rs. 7,50,001 to Rs. 10,00,000 | 15% |

| From Rs. 10,00,001 to Rs. 12,50,000 | 20% |

| From Rs. 12,50,001 to Rs. 15,00,000 | 25% |

| Above Rs. 15,00,000 | 30% |

Add:

- Surcharge: Surcharge is levied on the amount of income-tax at following rates if total income of the persons exceeds the specified limits:

| Surcharge | |

| Range of Income | Rate of Surcharge |

| A.Y. 2021-22 | |

| Rs. 50 Lakhs to Rs. 1 Crore | 10% |

| Rs. 1 Crore to Rs. 2 Crores | 15% |

| Rs. 2 Crores to Rs. 5 Crores | 25% |

| Exceeding Rs. 5 Crores | 37% |

Note: The enhanced surcharge of 25% & 37%, as the case may be, is not levied, from income chargeable to tax under sections 111A, 112A and 115AD (STCG, LTCG, Income of FIIs). Hence, the maximum rate of surcharge on tax payable on such incomes shall be 15%. However, marginal relief is available from surcharge.

- Health and Education Cess: @4% on the amount of income-tax plus surcharge.

Note: A resident individual (whose net income does not exceed Rs. 5,00,000) can avail rebate under section 87A. It is deductible from income-tax before calculating education cess. The amount of rebate is 100 per cent of income-tax or Rs. 12,500, whichever is less.

- Person has an option to opt for new tax regime or can continue to follow old tax regime.

The following are the key points highlighting the provision of Section 115BAC:

- Total income of the Individual or HUF under the new tax regime shall be computed without taking into account the following exemptions and deductions,

- Sec. 10(5): Leave Travel Concession

- Sec. 10(13A): House Rent Allowance

- Sec. 10(14): Specified allowances

- Sec. 10(32): Rs. 1500 per minor child in case of clubbing of his income

- Sec. 16(ia): Standard deduction of Rs. 50,000

- Sec. 16(ii): Entertainment Allowance

- Sec. 16(iii): Professional Tax Allowance

- Sec. 24(b): Interest on capital borrowed in respect of house property referred to in sec. 23(2) i.e. Self-occupied HP and Unoccupied HP

- Sec. 57(iia): Deduction for family pension

- All deductions covered in Chapter VI-A (i.e. 80C, 80D etc.) except those provided under section 80CCD(2) or 80JJAA or 80LA(1A) ( in case of Person, having a Unit in the International Financial Services Centre (IFSC), as referred in section 80LA(1A) )

- Sec. 10AA: Exemption for units in SEZ (Special Economic Zones)

- Sec. 32(1)(iia): Additional Depreciation

- Sec. 32AD: Deduction for new plant and machinery in notified backward areas

- Sec. 33AB: Deposit in Tea, Coffee, Rubber development account

- Sec. 33ABA: Site restoration fund

- Sec. 35(1)(ii)/(iia)/(iii)/35(2AA): Contribution for scientific research

- Sec. 35AD: Deduction for investment in specified business

- Sec. 35CCC: Expenditure on agricultural extension project

- Sec. 10(17): Exemption for certain income of MLAs, MPs

- Total income of the individual or HUF shall be computed without set off of, —

(a) Any Loss carried forward or unabsorbed depreciation from any earlier assessment years, if such loss or depreciation is attributable to any of the deductions/exemption referred above,

(b) Any Loss under the head "Income from house property" with any other head of income.

- Loss and depreciation referred above shall be deemed to have been given full effect to and no further deduction for such loss or depreciation shall be allowed for any subsequent year.

- Total income of the individual or HUF shall be computed without any exemption or deduction for allowances or perquisite.

- Option should be exercised by the person on or before the due date of furnishing return of income as mentioned u/s 139(1) of the Act.

- For Persons having income from business or profession, such option once exercised shall apply to subsequent assessment years and if withdrawn can’t opt for the option again in subsequent years.

- For Persons NOT having income from business or profession, such option can be exercised or withdrawn in any subsequent years.

- From the perspective of tax planning, it is essential to choose the tax regime at the beginning of the financial year. A taxpayer must make a comparison of the income tax under the new tax regime with the existing regime. Once the taxpayer chooses the tax regime at the beginning of the year, the investments and TDS or advance tax payable calculations are made accordingly.

Example 1:

| Particulars | Income (Rs) | Old regime (Rs) | New regime (Rs) | Tax Difference (Rs) |

| Salary | 12,50,000 | |||

| Less: Standard deduction | 50,000 | √ | ||

| Less: Professional tax | 2,400 | √ | ||

| Gross total income | 11,97,600 | |||

| Less: Deduction u/s 80C | 1,50,000 | √ | ||

| Total income | 10,47,600 | |||

| Income tax | 1,26,780 | 1,25,000 | ||

| Add: Education cess @ 4% | 5,071 | 5,000 | ||

| Total tax | 1,31,851 | 1,30,000 | 1,851 |

In Example 1, for a salary income of Rs 12,50,000, the new tax regime is marginally beneficial.

However, if assessee claim further deductions for health insurance, investment in NPS, interest on home loan and so on, the existing regime will be helpful.

(√ - Deduction is allowed)

Example 2:

| Particulars | Income (Rs) | Old regime (Rs) | New regime (Rs) | Tax Difference (Rs) |

| Salary | 10,00,000 | |||

| Less: Standard deduction | 50,000 | √ | ||

| Less: Professional tax | 2,400 | √ | ||

| Gross total income | 9,47,600 | |||

| Less: Deduction u/s 80C | 1,50,000 | √ | ||

| Total income | 7,97,600 | |||

| Income tax | 72,020 | 75,000 | ||

| Add: Education cess @ 4% | 2,881 | 3,000 | ||

| Total tax | 74,901 | 78,000 | -3,099 |

In Example 2, for a salary income of Rs 10,00,000, the existing tax regime is beneficial. In case an assessee claims lower deductions for tax savings, towards health insurance, investment in NPS and so on, the current system will be more beneficial.

However, if an individual claims a lower deduction of Rs 1 lakh under section 80C, then the new tax regime will be beneficial. It is important to note that each taxpayer should calculate income tax, taking into account their tax-saving investments and then choose the regime.

Disclaimer: It is suggested that user must cross-check all the facts, calculations, laws and contents of this software help with original Government Publications, Notifications & Circulars.

Related Blogs

All in one Software

- Income Tax Software

- TDS & TCS Software

- Audit e-filing Software

- CMA Data Software

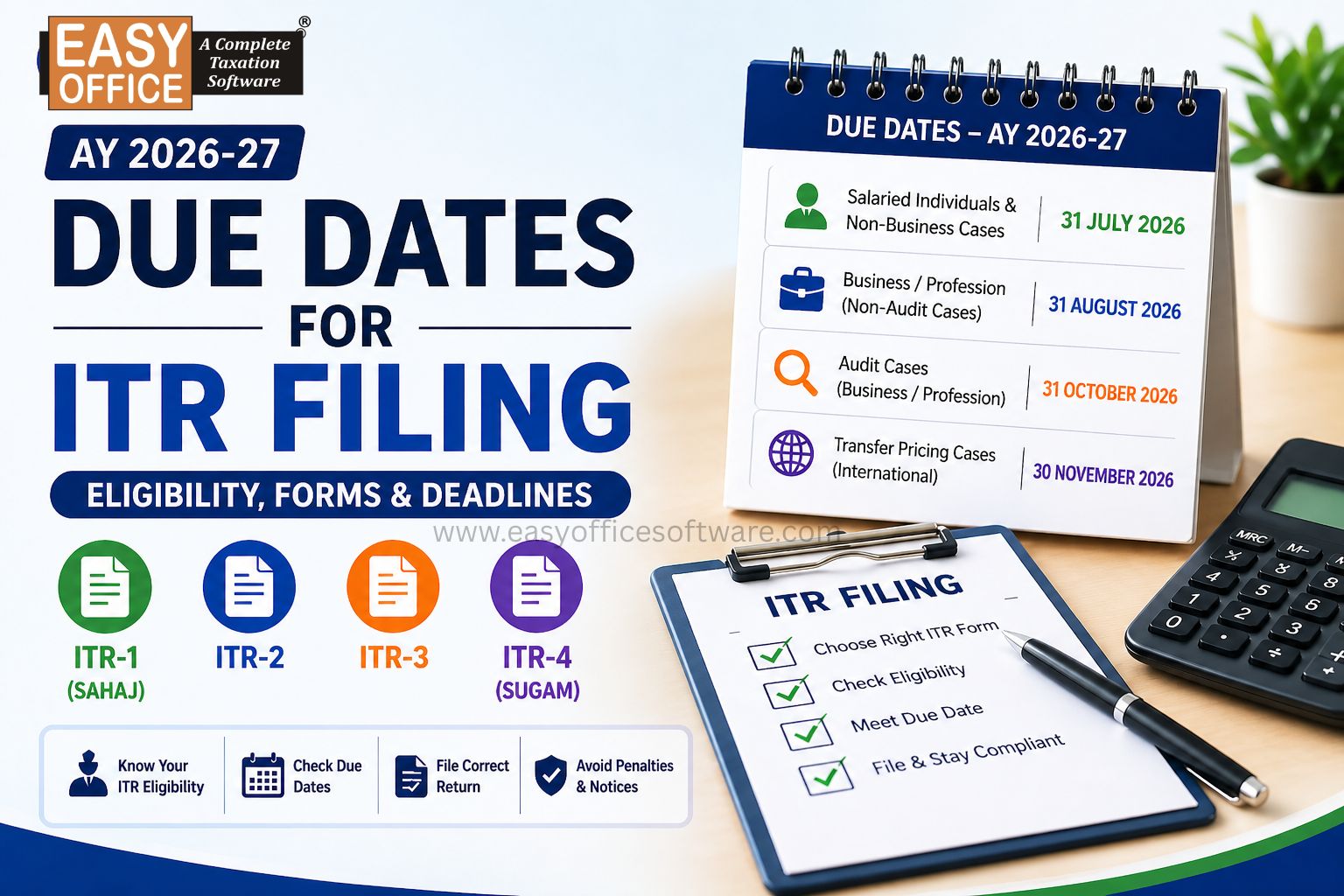

Penalty for Late Filing of Income Tax Return for FY 2025-26 – Section 234F of Income Tax Act 1961

#ITR