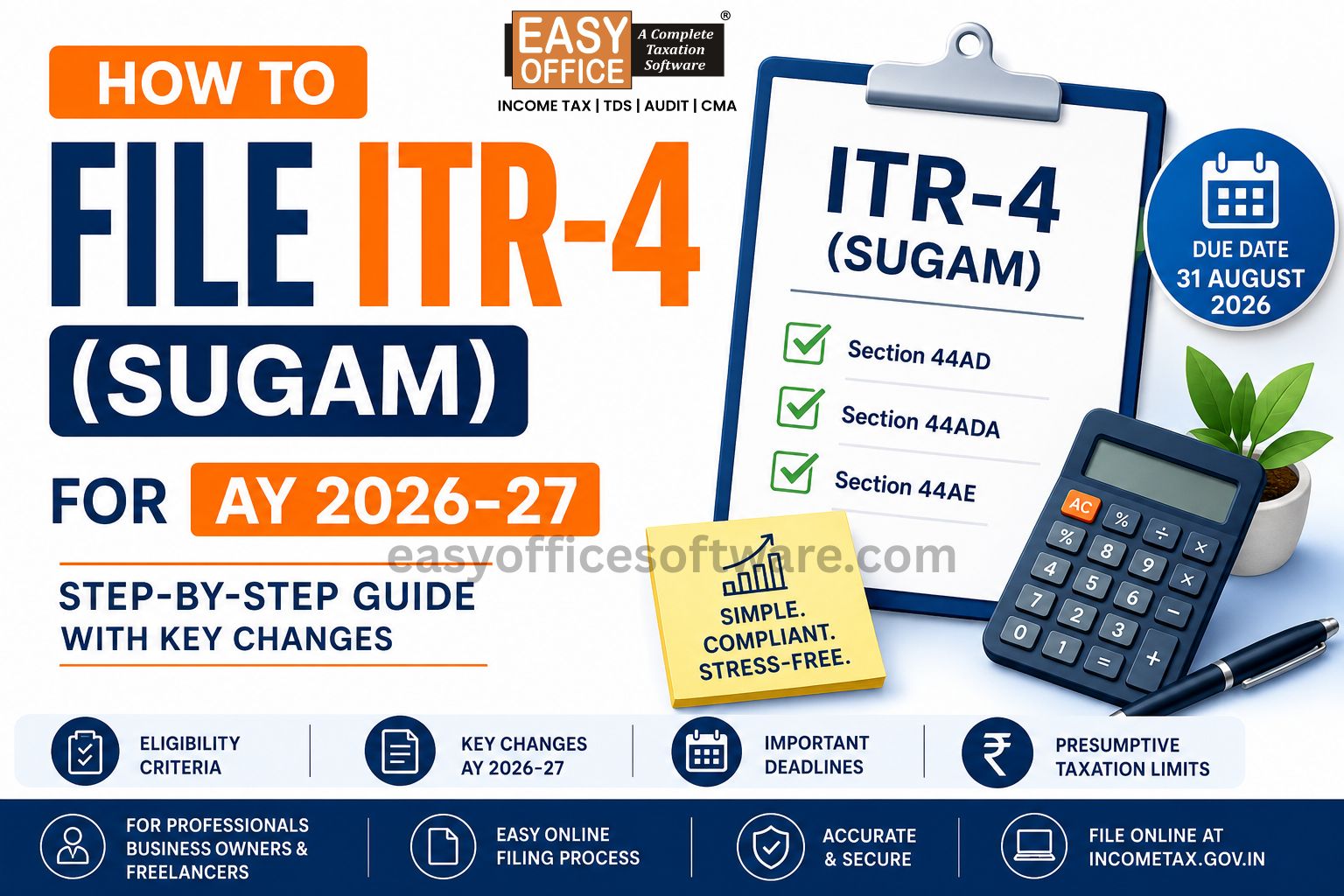

If you are a doctor, lawyer, architect, consultant, freelancer or small business owner opting for the Presumptive Taxation Scheme during FY 2025-26, this guide will help you with ITR filing using ITR-4 (Sugam) for AY 2026-27.

What is ITR-4 (Sugam)?

ITR-4 is a simplified form of income tax return for individual taxpayers, HUFs and partnership firms (excluding LLPs) opting for presumptive tax. Under the presumptive taxation scheme, eligible taxpayers are not required to maintain detailed books of accounts as per section 44 of Income Tax Act 1961. You declare a percentage of your business turnover or professional receipts as income and that is your taxable profit.

Eligibility Criteria for AY 2026-27

An ITR-4 can be filed when all these conditions are met:

Must be a Resident Indian. This form is not suitable for use by RNOR and NRIs.

Total income from all sources should be less than ₹50 Lakhs.

Must be earning income under the Presumptive scheme Section 44AD, 44ADA, or 44AE.

Salary/pension, income from up to two house properties, and other income (interest, family pension, etc).

Agricultural income not more than ₹5,000.

Presumptive taxation limits

| Section | Eligible taxpayer | Limit |

| 44AD | Businesses | ₹2 Cr / ₹3 Cr* |

| 44ADA | Professionals | ₹50L / ₹75L** |

| 44AE | Transporters | Maximum 10 vehicles |

| *Small businesses whose Cash receipts & payments ≤ 5% of turnover, otherwise ₹2 Cr. | **Specified professionals whose cash receipts & payments ≤ 5% otherwise ₹50 L. |

Who does not file ITR-4?

The following taxpayers are ineligible:

Companies and LLPs

Directors in any company

Holders of unlisted equity shares

Taxpayers with foreign assets or foreign-sourced income

Taxpayers with speculative business income (such as intraday trading) or F&O Income

Taxpayers with significant capital gains exceeding the relaxed limit of Section 112A (up to ₹1.25 Lakh) or any other capital gain not permitted.

Key Changes in ITR-4 for AY 2026-27

The following changes are made for this year. Before you begin filing, ensure you know all of them:

Two house properties: Income or loss from up to two house properties is permitted in ITR-4, compared to one earlier.

Mandatory bank closing balances: All active bank accounts must be disclosed with their closing balances as of 31 March 2026.

New ‘Investments’ field: on the assets side of the business balance sheet / financial particulars tab, an investment field has been added.

No Aadhar enrolment ID: The portal is no longer accepting a 28-digit Aadhaar Enrolment ID. Only a 12-digit Aadhaar Card Number is valid.

New Tax Regime is the default: In case of business or professional income, you must submit Form 10-IEA on or before the due date to choose the Old Tax Regime.

Documents to keep handy

The ITR-4 is an annexure-less form, meaning that no attachments are to be made. However, keep these,

PAN and Aadhaar (must be linked to each other)

AIS (Annual Information Statement) and TIS (Taxpayer Information Summary) to ensure turnover and interest income are accurate

26AS (to check TDS and TCS credits)

Bank statements - to differentiate digital vs. cash receipts (especially important for the 5% cash rule)

Step-by-Step Filing Guide

1.Log in to the e-filing portal

Visit incometax.gov.in and log in with your PAN/Aadhaar and password.

2. Start your return

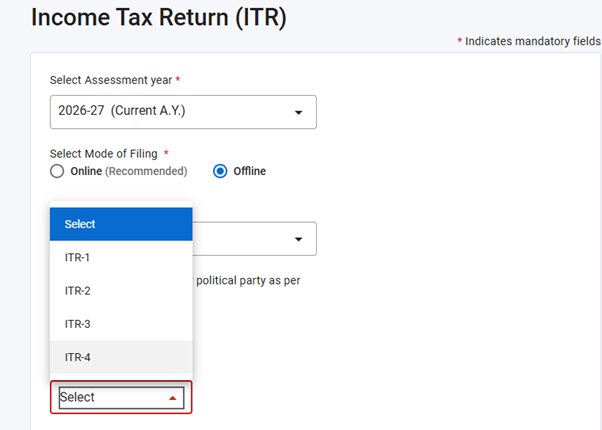

Go to e-File > Income Tax Returns > File Income Tax Return. Select Assessment Year AY 2026-27 and choose Online mode.

3. Select your status and form

Select Individual or HUF and then ITR-4 (Sugam) from the form drop-down.

4. Choose reason for filing

Choose the correct reason, usually “Taxable income is above basic exemption limit.”

5. Fill and review all schedules

Personal Info: Check pre-filled information and tax regime.

If choosing the Old Regime, submit File Form 10-IEA here.

Schedule BP: Declare gross turnover and presumptive profit (6% digital / 8% cash for less than 44AD; 50% gross receipts under 44ADA).

Financial Particulars: Enter the cash balance, bank closing balances, investments, and inventory.

Deductions: Claim the deduction under 80C, 80D, etc., through the new dropdown structure

6. Review taxes paid

Check if the pre-filled TDS, TCS, and advance tax are correct. If any self-assessment tax is due and has not yet been paid, do so online before you continue.

7. Preview and validate

Look through the whole return. Click on Proceed to Validation and check for any errors that are marked by the system.

8. e-Verify immediately

Click on Proceed to Verification and e-verify via Aadhaar OTP/Net banking/Bank Account EVC. Failure to e-verify your return for 30 days from filing will render it invalid for return.

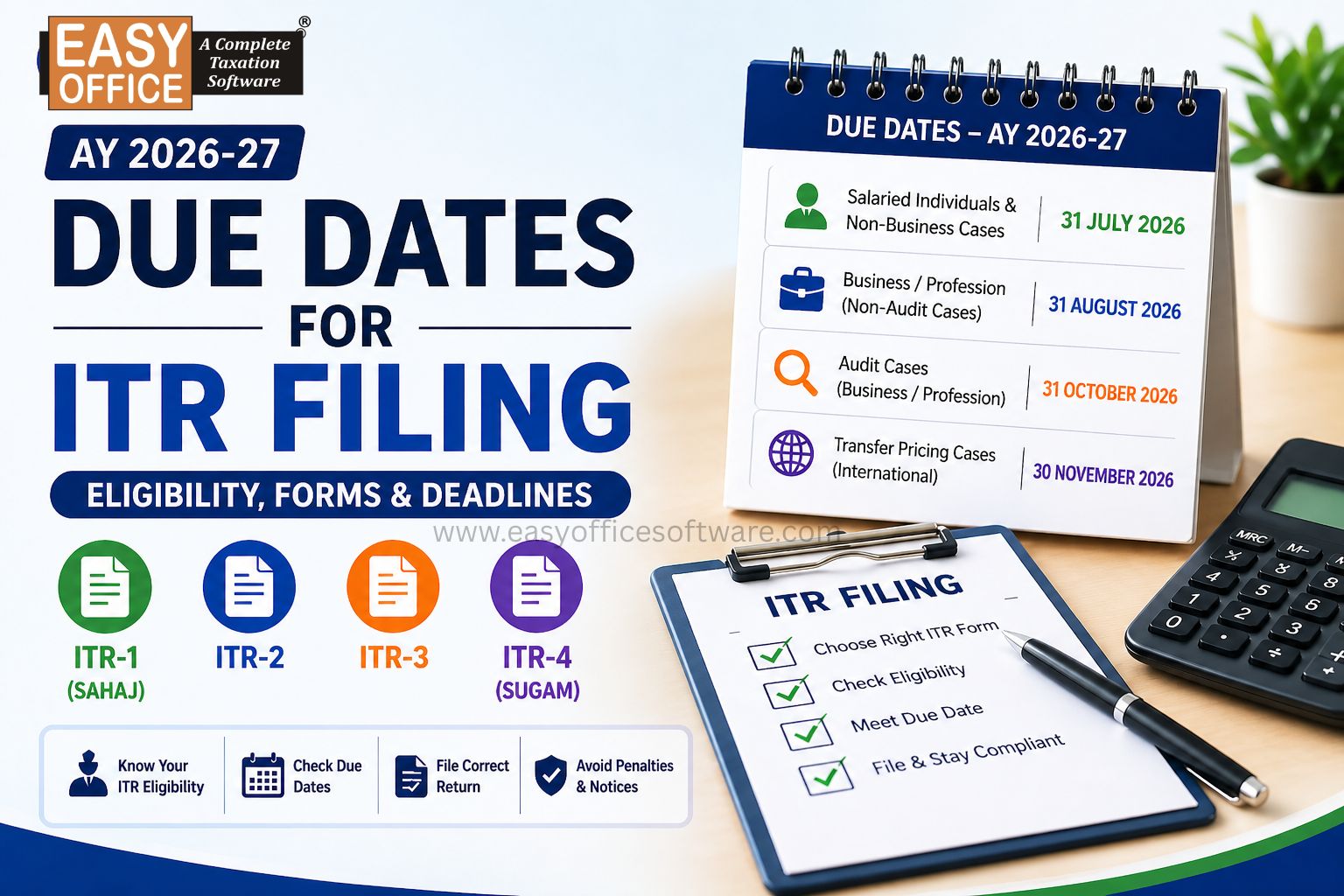

Important Deadlines

Original filing (non-audit) 31 August 2026 | Belated 31 December 2026 | Revised return 31 March 2027 |

Any late filing of forms after 31 August 2026 will incur a fine of up to ₹5,000/1,000.

Common Mistakes While Filing ITR-4

Choosing wrong ITR form

Forgetting Form 10-IEA or Filing after Due date

Wrong turnover

Missing bank accounts

Not reconciling AIS / Form 26AS

Forgetting e-verification

Conclusion

Filing ITR-4 is simple when you understand your eligibility under the presumptive taxation scheme. Before filing, verify your turnover, bank details, AIS, Form 26AS and tax regime selection. If your income includes capital gains, foreign assets, or multiple businesses, consult a Chartered Accountant before filing.

Pro Tip for Tax Professionals: Integrated tax software such as EasyOFFICE helps automate ITR-4 preparation by importing taxpayer data, validating entries, reconciling Form 26AS/AIS/TIS and reducing manual errors during filing.

FAQs

Q. Who can file ITR-4 (Sugam) for AY 2026-27?

ITR-4 form is to be filled by individuals, Partnership Firms (not LLP), where total income is less than or equal to ₹50 Lakhs and opting for Presumptive Taxation Scheme (section 44AD or 44ADA or 44AE).

Q. When is the ITR-4 Due date for AY 2026-27?

The due date for filing ITR-4 (non-audit cases) for AY 2026-27 is 31 August 2026. A belated/revised return under Section 234F can be submitted till 31 December 2026/ 31March 2026 respectively with a maximum amount of late fee that would be levied at ₹ 5,000/1,000 per return.

Q. What is the maximum limit for turnover in Section 44AD for the AY 2026-27?

As per section 44AD, the turnover limit is set as ₹2 Crore. If the cash receipts & payments comprise not more than 5% of the turnover, then the limit is increased to ₹3 Crore. Digital receipts are charged at 6% and cash receipts at 8%.

Q. Which documents are needed to file ITR-4?

ITR-4 doesn't involve attaching an Annexure, so there is no document to attach. However, it is imperative that PAN and Aadhaar, along with Form 26AS, AIS/TIS, and bank statements, should be readily available to ensure proper filling of the form and to be able to make a cross-check of the details that have been pre-filled.

Related Blogs

All in one Software

- Income Tax Software

- TDS & TCS Software

- Audit e-filing Software

- CMA Data Software

Penalty for Late Filing of Income Tax Return for FY 2025-26 – Section 234F of Income Tax Act 1961

#ITR