The Finance Minister Nirmala Sitharaman has proposed several major direct tax system modifications during her Union Budget 2026–27 presentation to the Lok Sabha.

This marks her ninth consecutive Union Budget. The government has confirmed that the new Income Tax Act, 2025, will come into force on 1 April 2026, as the legislation will replace the Income Tax Act of 1961.

The objective is clear. Simplify tax laws, reduce disputes, and make tax compliance easier for individuals and businesses.

This reform signals a shift from incremental amendments to structural simplification. We have mentioned the precise income tax highlights from Budget 2026-27.

1. New Income Tax Act, 2025 from April 2026

The government will replace the 1961 Act with a rewritten Income Tax Act, 2025. The new law focuses on clarity rather than changing tax rates. The sections have been simplified by reducing their cross-references.

The government wants to make the law simpler so that people and businesses can understand it better. The government expects this change to lower litigation and improve voluntary compliance.

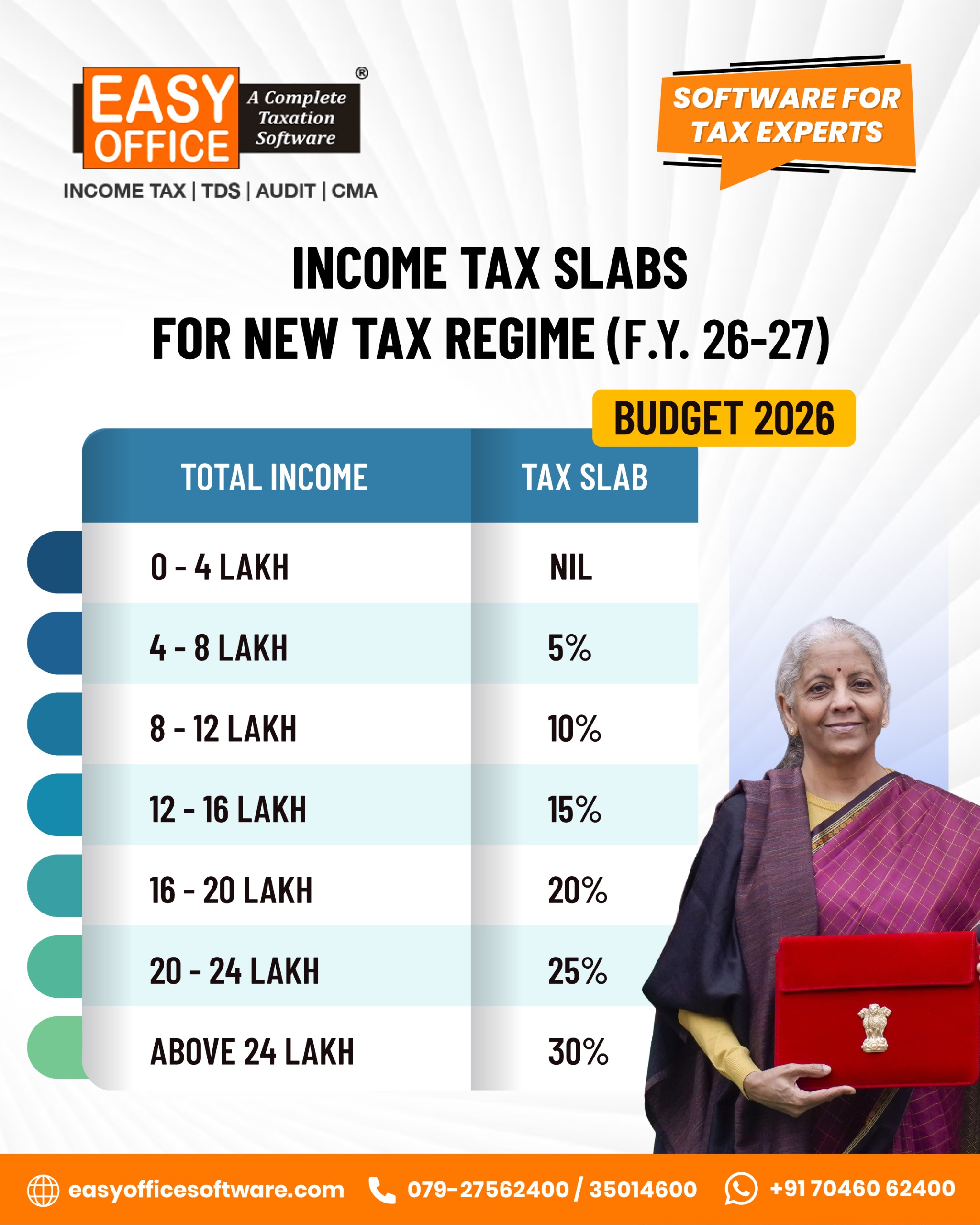

The Budget 2026 announcement did not include any modifications to income tax slabs or exemption limits.

2. Revised Return timeline extended

Budget 2026 proposes extending the deadline for revised returns.

| Return Type | Earlier Deadline | New Deadline |

|---|---|---|

| Revised Return | 9 months from year-end | 12 months from year-end |

| Belated Return | 9 months from year-end | No change |

The new rule permits taxpayers who submitted their tax returns after the deadline to fix their errors. Earlier, late filers lost this opportunity. This proposal improves fairness for all parties involved while preventing any party from postponing their responsibilities.

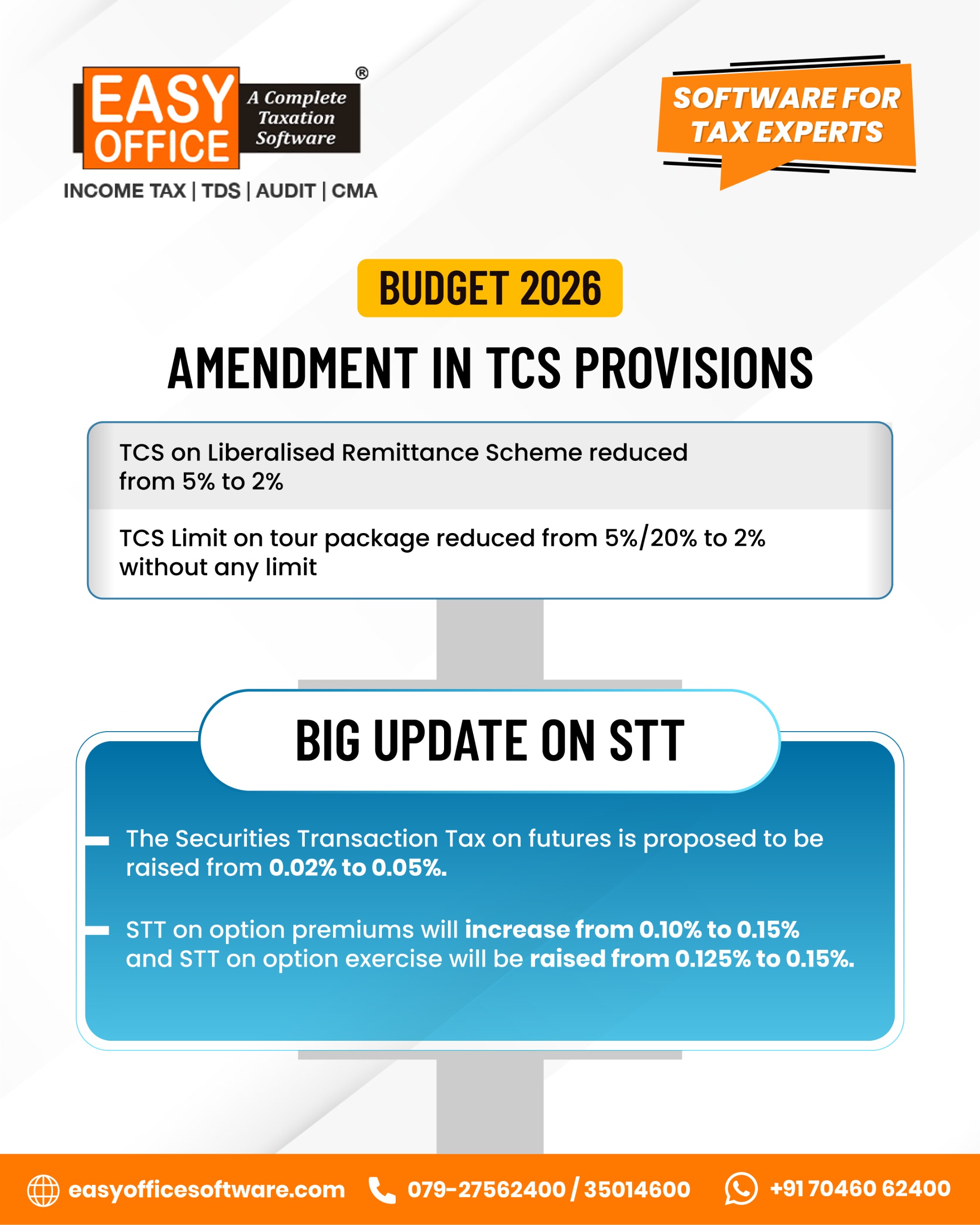

3. TCS reduced on overseas education and medical remittances

The Tax Collected at Source (TCS) for the Liberalized Remittance Scheme has been reduced.

| Purpose | Earlier TCS | New TCS (from April 1, 2026) |

|---|---|---|

| Overseas education | 5% | 2% |

| Medical treatment abroad | 5% | 2% |

The relief program provides financial benefits to families who are paying for international education and healthcare expenses. The government confirmed that this measure does not qualify as a tax exemption. The adjustment process will remain active until the completion of the return filing.

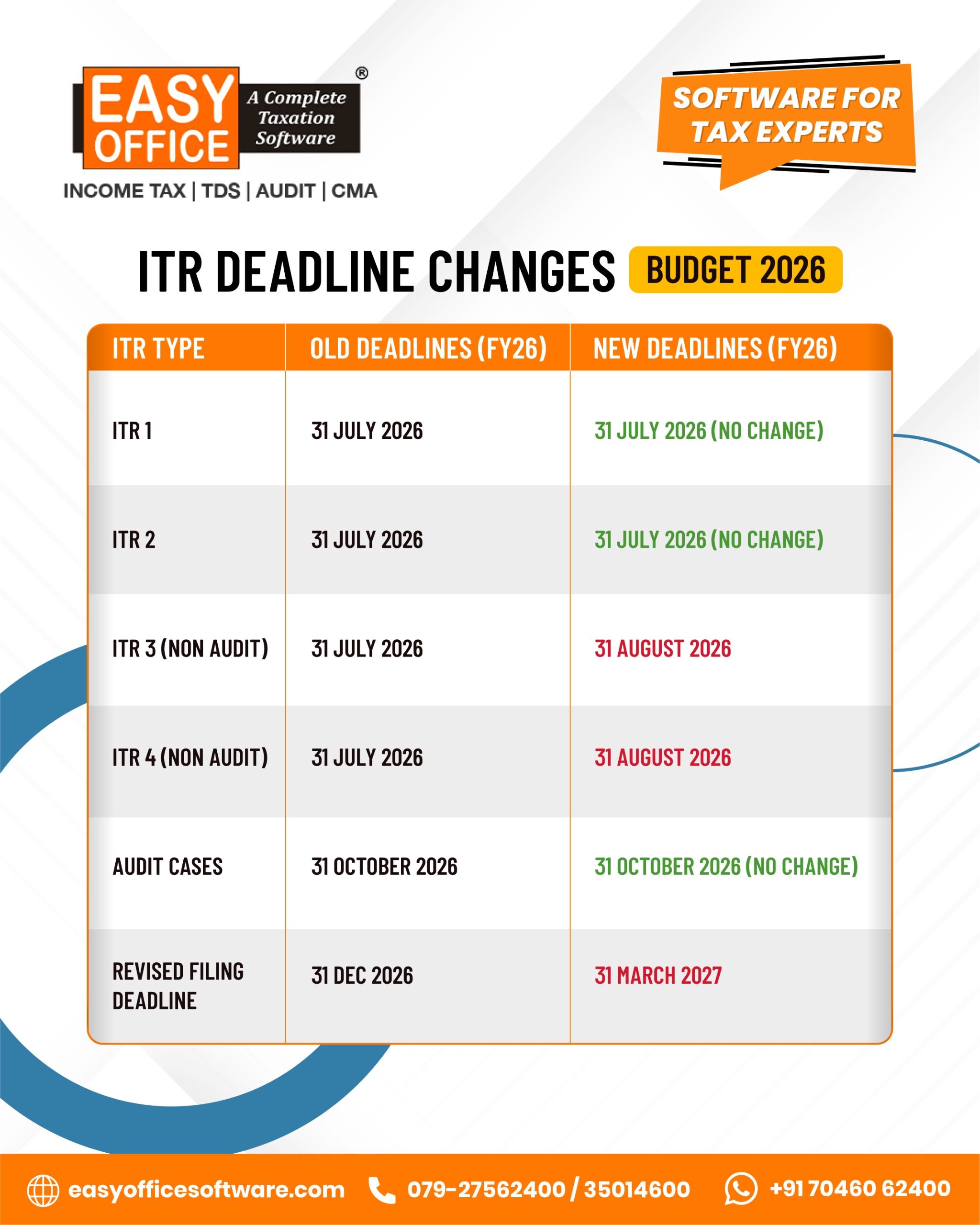

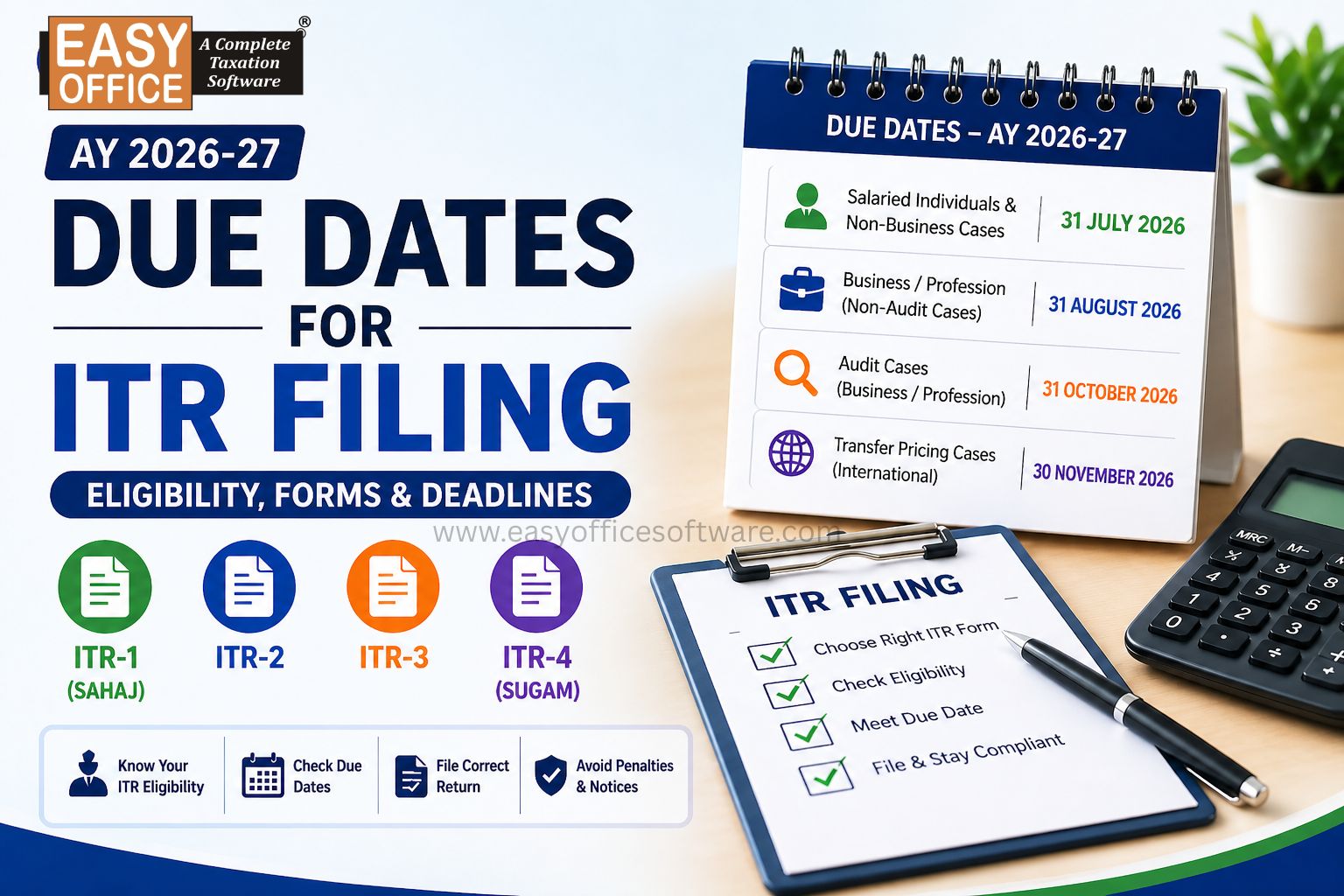

4. Clarity on ITR due dates

The government stated the filing deadlines, which help people understand better without any confusion.

| Taxpayer Category | Due Date |

|---|---|

| ITR-1 and ITR-2 | 31 July |

| Non-audit taxpayers | 31 August |

| Revised returns | 31 March |

This ensures expected outcomes and prevents frequent deadline extensions.

5. Changes in equity derivatives taxation

The Security Transaction Tax on equity derivatives increased through Budget 2026.

| Instrument | Earlier STT | Revised STT |

|---|---|---|

| Equity futures | 0.02% | 0.05% |

| Equity options | 0.10% | 0.15% |

The change results in higher costs for trading activities. The government intends to reduce speculative trading through its current implementation.

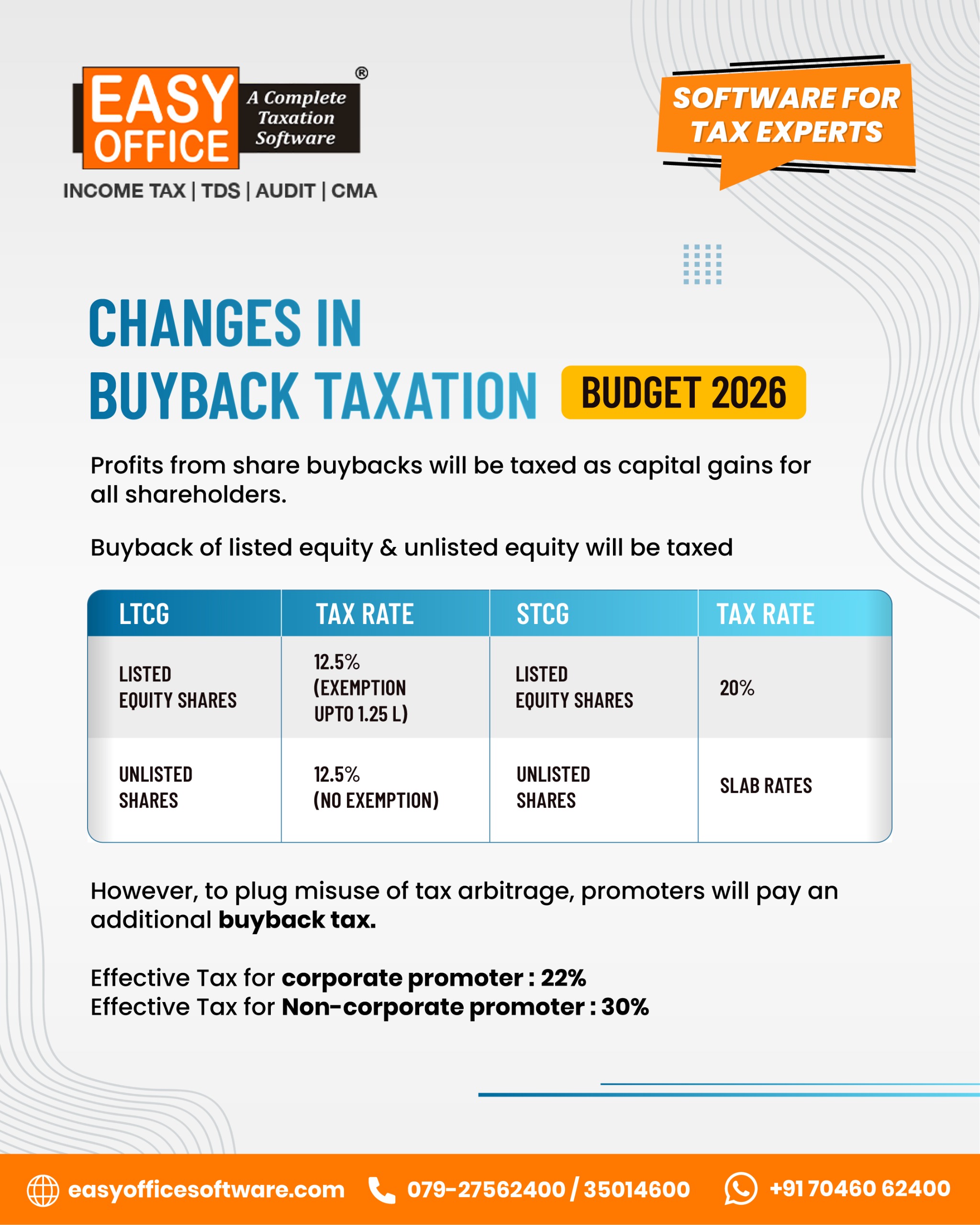

6. Buyback Taxation Recast to Protect Minority Shareholders

The taxation of share buybacks has been redesigned in Budget 2026. Buyback proceeds will now be treated as capital gains rather than income from other sources. The new tax system protects minority shareholders by applying taxes only to their total earnings.

The tax system requires corporate promoters to pay 22% and non-corporate promoters to pay 30 % as effective tax rates to maintain fairness and prevent tax arbitrage.

7 . Corporate Tax Reset: MAT Becomes Final Tax

The 2026 budget introduces a fundamental change to corporate taxation by making Minimum Alternate Tax (MAT) the final tax from 1 April 2026. The MAT rate decreases to 14% from its previous rate of 15%, while no further MAT credit accumulates after this point.

The existing MAT credit up to 31 March 2026 can be used. The new tax regime provides MAT credit set-off, which businesses can use to offset 25% of their yearly tax obligations.

8. Sovereign Gold Bond tax rule clarified.

The capital gains exemption for SGB redemption will only benefit investors who purchase bonds at their original RBI issue prices and hold them until maturity.

The secondary market buyers who acquire this exemption will face capital gains tax. The clarification has eliminated the long-standing ambiguity.

9. One-time foreign asset disclosure scheme

The government plans to establish a six-month voluntary disclosure.

| Taxpayer Category | Asset Limit | Compliance Cost |

|---|---|---|

| Fully non-compliant | Up to ₹1 crore | Tax plus penalty substitute |

| Partially compliant | Up to ₹5 crore | ₹1 lakh fee |

The scheme targets small taxpayers, students, salaried individuals, and NRIs. The program protects individuals who choose to comply with its requirements.

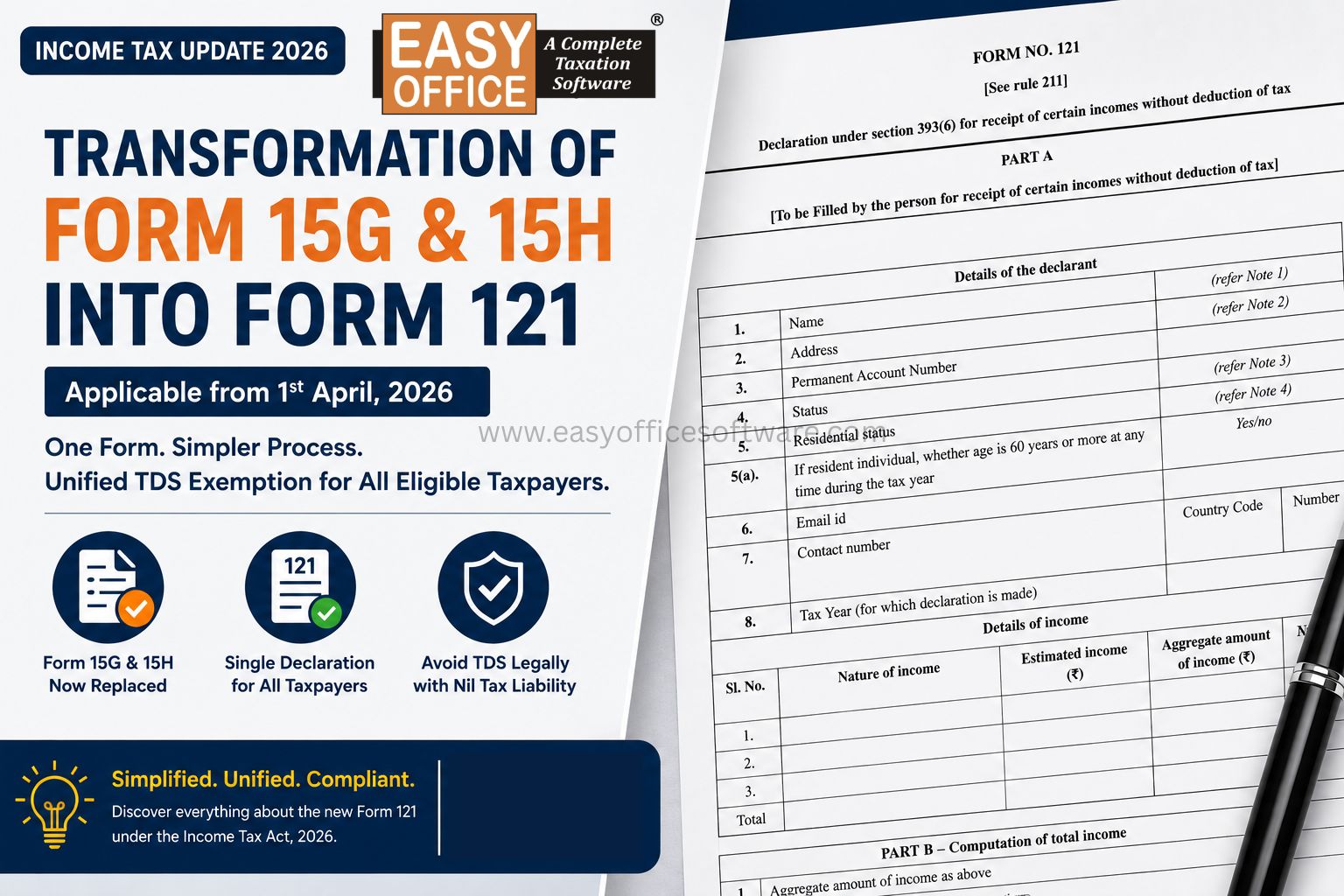

10. Easier Form 15G and 15H handling

Depositories will now accept Form 15G and Form 15H and forward them to companies directly. The process of compliance becomes easier for investors who possess securities from different companies.

The automatic system will provide small taxpayers with TDS certificates that show lower or nil TDS. The need for manual applications to assess officers will reduce.

Technology and AI-driven tax administration

India is uniquely prepared for technology and AI-driven tax transition because its digital tax system functions as its main strength. The platforms GSTN, e-invoicing, AIS, TIS, PAN–Aadhaar linkage, and faceless assessments have improved data quality. It has widened the tax base and accelerated processing. The current state of digital development enables tax authorities to use artificial intelligence for better compliance monitoring.

AI technology is revolutionizing tax operations through its ability to manage document assessments, draft responses to notices, detect potential compliance issues, and explain intricate tax regulations.

For example, and AI integrated income tax filing software can take a few seconds to offer enhanced precision and stable outcomes in tax filing. Tax compliance has shifted from annual reactive filing to a reactive filing toward continuous and proactive management.

A strong emphasis is placed on responsible AI adoption. This approach includes verified data, traceable logic, and a ‘human-in-the-loop’ model to function properly. The AI system aids in decision-making processes, but legal accuracy depends on professional judgment.

The smart technology enables better expertise, improving audit readiness, strengthens compliance confidence throughout India.

Concluding…

The Union Budget 2026-27 brings changes to income tax administration without altering slabs. The change involves fundamental alterations instead of surface-level modifications. The new system will depend on automated processes, which will deliver precise results for its compliance requirements.

Understanding these changes early is critical. Taxpayers who use Income tax filing software experience faster adaptation to the new tax regulations. The need for Income tax filing software like EasyOFFICE becomes mandatory because systems are transforming into AI-controlled operations.

Union Budget 2026, Income Tax Highlights, Indian Tax Reforms, TCS Changes 2026, Tax Compliance India, GST & Tax Updates, Taxpayer Relief, Budget News

All in one Software

- Income Tax Software

- TDS & TCS Software

- Audit e-filing Software

- CMA Data Software

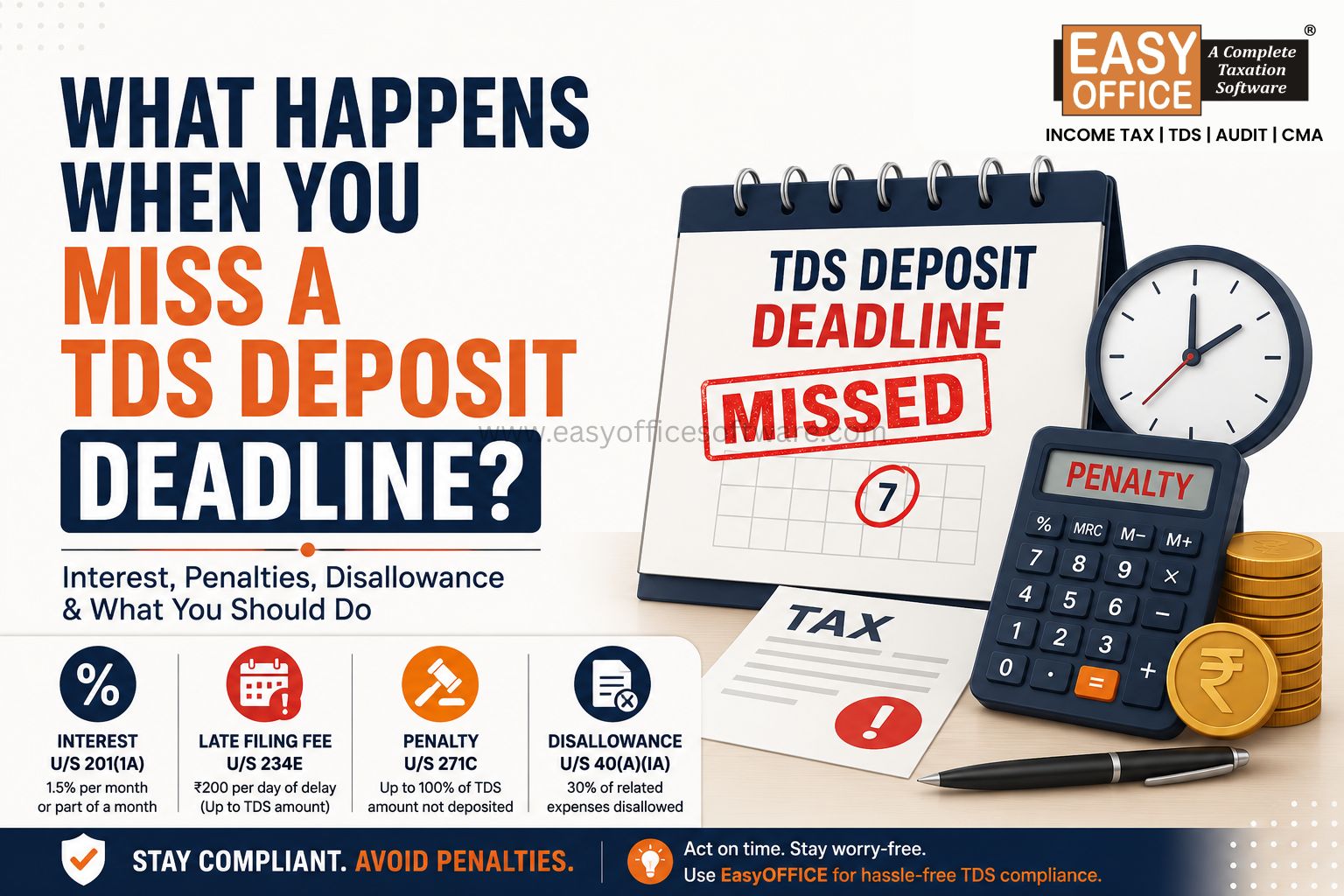

Penalty for Late Filing of Income Tax Return for FY 2025-26 – Section 234F of Income Tax Act 1961

#ITR