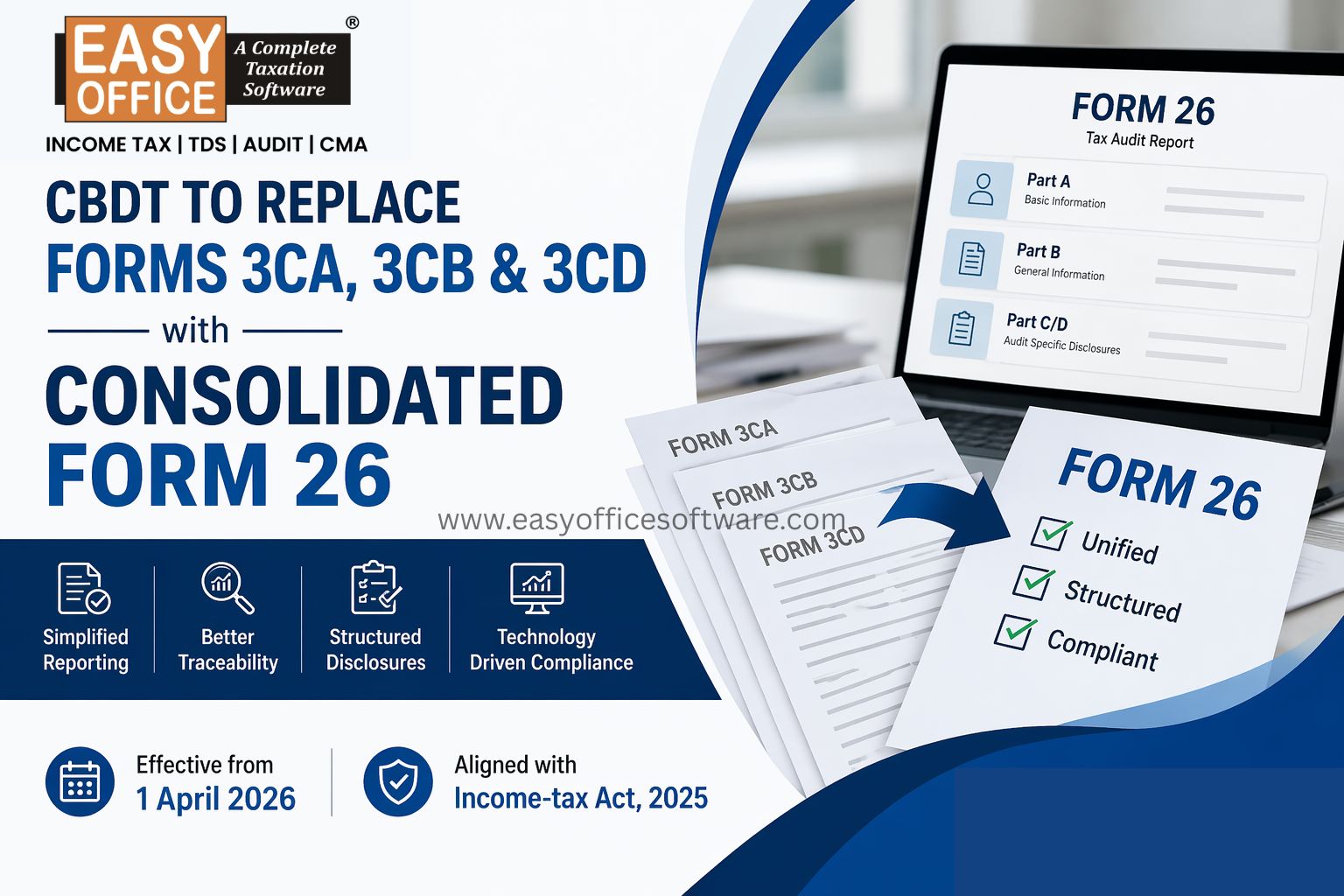

Introduction

For more than 60 years, Form 16 was the most important piece of paper for every salaried Individual. However, it will now be replaced by Form 130 under the new Income Tax Act 2025 from the Tax year 2026-27, focusing on the digital age. Here is everything you need to know about this transformation, and how it might affect you.

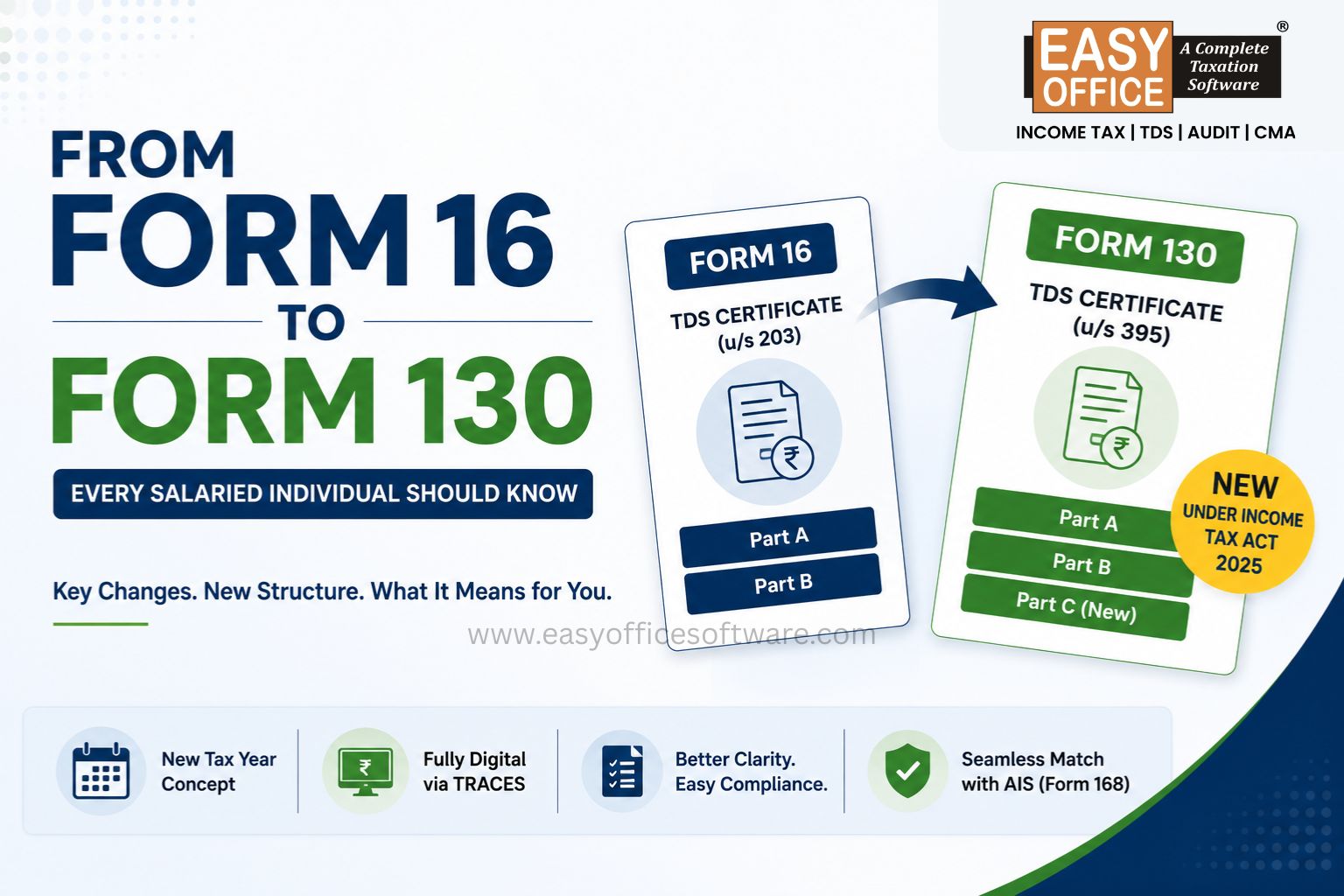

What is Form 16?

Form 16, u/s 203 of the Income Tax Act 1961, is a TDS certificate that an employer issues to each employee each year. It is a formal document stating the amount of TDS that has been deducted from the employee’s salary by the employer and paid to the government. Form 16 consisted of two parts - Part A and Part B, generated from Traces Portal.

What is Form 130?

Form 130 serves the same purpose, i.e., to confirm that TDS has been deducted and paid. The due date for issuance also remains the same. It differs from Form 16 as it contains 3 parts- Part A, Part B, and Part C (new).

Part A is more or less similar to the Form 16, with a few fields renamed or expanded in detail. (Employer and Employee Basic details)

Old Part B's salary computation has moved into the new Part C Annexure I, making your full income picture cleaner, consolidated and pre-computed in one place.

New Part B contains the information regarding total salary paid and a summary of TDS deducted and deposited throughout the year.

The new part is Part C's Annexure II, which is specific to employees who are senior citizens (60+) for pension and interest income under Section 393 (those who have not filed an ITR). For those employees, Form 130 shall be value adding.

Why did we need to leave Form 16?

• The aging Income Tax Act of 1961 created a fragmented, confusing compliance system centered around the manual-era Form 16.

• Form 16 used a non-consequential approach and "Previous" vs. "Assessment" year labels, making comprehension difficult.

• The Income Tax Act 2025 introduced Form 130 to replace its predecessor.

• Form 130 provides a standardized, machine-readable format optimized for AI-driven analytics and modern data compliance

Form 16 vs Form 130: The key differences

| Form 16 (old) | Form 130 (new) |

| Governed by Section 203, Income Tax Act, 1961 | Governed by Section 395, Income Tax Act, 2025 |

| 2 parts: Part A (TDS summary) and Part B (Salary details) | 3 parts: Part A, Part B and new Part C (full income computation) |

| Referenced "Previous Year" and "Assessment Year" - two separate labels | References a single "Tax Year" - one label for earning and filing |

| Could be issued offline in some cases | Must be issued compulsorily through the TRACES portal - no offline issuance permitted |

| Senior citizen provisions are covered separately | Annexure II in Part C specifically covers pension and interest income for senior citizens under Section 393 |

| Limited integration with AIS; reconciliation was manual | Designed for seamless AI-driven reconciliation with the Annual Information Statement (now Form 168) |

| Form 16A for non-salary TDS (rent, interest, professional fees) | Form 16A renamed to Form 131 |

The broader Form renumbering: a new tax vocabulary

| OLD FORM | NEW FORM* | PURPOSE |

| Form 16 | Form 130 | TDS certificate for salary income |

| Form 16A | Form 131 | TDS certificate for non-salary income |

| Form 26AS | Form 168 | Annual Information Statement (tax credit) |

| Form 10F | Form 41 | Tax Residency Certificate application (DTAA) |

| Form 12BB | Form 124 | HRA, home loan interest, LTC declarations |

| (New) | Form 122 | Previous employer TDS declaration in case of multiple employers |

*New Form numbers subject to notification under Income Tax Act, 2025

What this means for employees?

For most employees, the change is not much in practice; it is designed that way. You will get a document from HR for Tax Year 2026-27 (FY 2026-27) that is a bit different from what you had in the past - an additional Part C.

• Remember to verify your salary, TDS deducted and exemptions in Form 130 exactly as you did with Form 16

• Cross-check against Form 168 (the new Form 26AS) to ensure TDS credits match

• Submit Form 122 to your employer before April 2026 payroll - declaring tax regime choice and previous employer TDS

• Use Form 124 (replacing Form 12BB) to declare HRA, home loan interest and Leave Travel Allowances

• Note that Form 130 cannot be issued offline - it must come through the TRACES portal

• If you changed jobs during the year, collect a separate Form 130 from each employer

What this means for Employers and HR teams?

The transition is most challenging for payroll and HR managers.

Offline issuance is prohibited. The new three-part Form 130 must be created and issued only via the TRACES portal by all employers.

The new Act applies based on payment or credit dates. Form 16 covers March 2026 payments, but April 2026 is governed by the new Act.

Teams need to fine-tune April payrolls for precise reporting across this compliance junction.

Conclusion

For sixty years, Form 16 stood tall in India. Form 130 is its proud successor - a new form, same functionality. Make sure to check your figures, understand the structure and always be tax-informed. Because India has upgraded its tax system, it's now time for you to catch up.

FAQs

Q. I just received my Form 16 for FY 2025–26. Do I need to do anything differently this year because of the new law?

A. No - this year's filing is completely unchanged. The Income Tax Act, 2025, applies to income earned from April 1, 2026, onwards. For now, proceed normally

Q. Form 130 has three parts instead of two — what is actually new in Part C, and do I need to worry about it?

A. Annexure II within Part C applies only to a specific group: senior citizens above 60 who receive a pension or interest income and have opted not to file an ITR under Section 393. If you are a regular salaried employee below 60, Annexure I in Part C is what applies to you, and it simply gives you a clearer, pre-computed picture of your tax position.

Q. What should I do if I change jobs mid-year?

A. Same as before, you must collect Form 16 with Part A and Part B from the previous employer for the period you have worked with them. From the current employer, collect Form 130 with Part A, Part B and Part C.

Q. How does TDS Software help employers comply with Form 130 and the updated salary TDS reporting rules?

A. EasyOFFICE – TDS Software helps employers and tax professionals comply with Form 130 and the updated salary TDS framework by automating the entire salary TDS lifecycle - from deduction to reporting and correction.

The software calculates salary TDS accurately under the Tax Year concept, validates PAN -salary linkage, generates challans and TDS returns, and supports online correction workflows through TRACES. This ensures timely issuance of salary TDS certificates, reduces mismatches with AIS and Form 168 and minimizes the risk of notices, penalties or reconciliation errors.

TDS Return Filing, TDS Software, EasyOFFICE, Form 130

Related Blogs

All in one Software

- Income Tax Software

- TDS & TCS Software

- Audit e-filing Software

- CMA Data Software

Penalty for Late Filing of Income Tax Return for FY 2025-26 – Section 234F of Income Tax Act 1961

#ITR