TDS (Tax Deducted at Source) is one of the most critical compliance areas under the Income Tax Act. Whether you are a business owner, HR professional, Chartered Accountant, or tax consultant, staying updated with the latest TDS rates for FY 2025-26 is essential to avoid penalties, interest, and departmental notices.

With increasing digitisation and data matching by the Income Tax Department, manual TDS calculations have become highly risky. This is where online TDS return filing software plays a vital role by ensuring accurate deduction, timely payment, and seamless return filing.

Let us break down the TDS rates applicable for FY 2025-26 section-wise, along with practical insights and key compliance considerations.

Why TDS Rates Matter for FY 2025-26

TDS compliance is not limited to deduction alone—it requires correct deduction under the correct section and at the correct rate. Even a minor error can result in:

» Interest under Section 201

» Late fees under Section 234E

» Notices from the Income Tax Department

A significant number of TDS-related notices are issued due to incorrect rate application or wrong section selection. Referring to an updated TDS rates chart for FY 2025-26 helps mitigate these risks effectively.

What Is TDS and How It Works

TDS refers to tax deducted at the time of making specified payments such as salary, rent, professional fees, interest, commission, and similar transactions.

The deductor is responsible for the following:

» Deducting tax at applicable rates

» Depositing TDS within prescribed timelines

» Filing quarterly TDS returns

» Issuing TDS certificates

Using online TDS return filing software significantly simplifies and automates these compliance requirements.

Key Highlights of TDS for FY 2025-26

For FY 2025-26, most TDS rates remain unchanged; however, regulatory scrutiny has intensified. Key highlights include:

» Strict enforcement of higher TDS in non-PAN cases

» Continued applicability of Section 206AB for non-filers

» Extensive use of AIS and Form 26AS for data matching

Automation is no longer optional – it has become essential.

TDS Rates Chart for FY 2025-26 (Section-wise Overview)

The TDS framework is structured section-wise, with each section specifying:

I. Threshold limit

II. Applicable rate

III. Defined nature of payment

Understanding this structure is critical before making any TDS deduction.

1. TDS on Salary – Section 192

TDS on salary is calculated based on estimated annual income after considering applicable exemptions and deductions.

Key points:

I. No fixed rate

II. Based on applicable income tax slabs

III. Employer is required to issue Form 16

Errors in salary TDS are among the leading causes of employee grievances and mismatches in Form 26AS.

2. TDS on EPF Withdrawal – Section 192A

If EPF is withdrawn before completion of five years of continuous service and the amount exceeds ₹50,000, TDS becomes applicable.

Applicable rates:

I. 10% with PAN

II. 20% without PAN

This provision is often overlooked, resulting in unexpected deductions for taxpayers.

3. TDS on Interest on Securities – Section 193

Applicable on interest income from debentures and government securities.

Rate: 10% (subject to prescribed threshold limits in certain cases)

4. TDS on Dividend Income – Section 194

Dividend income is taxable in the hands of shareholders.

Rate: 10% where dividend income exceeds ₹5,000

Investors should monitor this closely to avoid mismatches while filing returns.

5. TDS on Interest Other Than Securities – Section 194A

Applicable on interest earned from:

- Fixed deposits

- Recurring deposits

- Loans

Rate: 10%

Threshold: ₹40,000 for individuals and ₹50,000 for senior citizens

This is one of the most frequently applied TDS sections by banks and NBFCs.

6. TDS on Winnings and Online Gaming – Sections 194B & 194BA

Applicable on winnings from lotteries, betting, and online gaming.

I. Rate: Flat 30%

II. Threshold: ₹10,000 under Section 194B; no threshold under Section 194BA (online gaming)

7. TDS on Contractor Payments – Section 194C

Widely applicable across business transactions.

Rates:

I. 1% for Individuals/HUF

II. 2% for others

Threshold: ₹30,000 per contract or ₹1,00,000 annually

Incorrect section selection under this provision is a common compliance error.

8. TDS on Insurance Commission – Section 194D

Applicable to insurance commission payments.

I. Rate: 2% for Individuals/HUF and 10% for companies

II. Threshold: ₹20,000

9. TDS on Commission or Brokerage – Section 194H

Applicable to commission or brokerage payments excluding insurance commission.

Rate: 2%

Threshold: ₹20,000

10. TDS on Rent – Sections 194I and 194IB

For businesses, Section 194I applies:

» 2% on plant and machinery

» 10% on land, building, furniture, or fittings

For Individuals/HUF not liable to tax audit, Section 194IB applies at a flat 2% where rent exceeds ₹50,000 per month.

11. TDS on Property Purchase (Other Than Agricultural Land) – Section 194IA

Applicable where the property value exceeds ₹50 lakh.

Rate: 1%

12. TDS on Professional and Technical Fees – Section 194J

Applicable on payments made to professionals such as CAs, lawyers, doctors, consultants, and technical experts.

I. Rate: 10% for professional fees and 2% for technical services

II. Threshold: ₹50,000

13. TDS on E-commerce Transactions – Section 194O

Applicable to e-commerce operators.

Rate: 0.1%

Threshold: ₹5 lakh for Individuals/HUF

14. TDS on Purchase of Goods – Section 194Q

Applicable to buyers whose turnover exceeds ₹10 crore.

Rate: 0.1%

Threshold: Purchases exceeding ₹50 lakh

15. TDS on Virtual Digital Assets – Section 194S

Applicable to transactions involving cryptocurrencies and NFTs.

Rate: 1%

Threshold: ₹10,000 for others and ₹50,000 for specified persons

This section is closely monitored by the Income Tax Department.

Higher TDS for Non-PAN and Non-Filers

In cases where PAN is not furnished, higher TDS is applicable under Section 206AA.

Non-filers of income tax returns are subject to higher TDS under Section 206AB, significantly increasing compliance obligations for businesses.

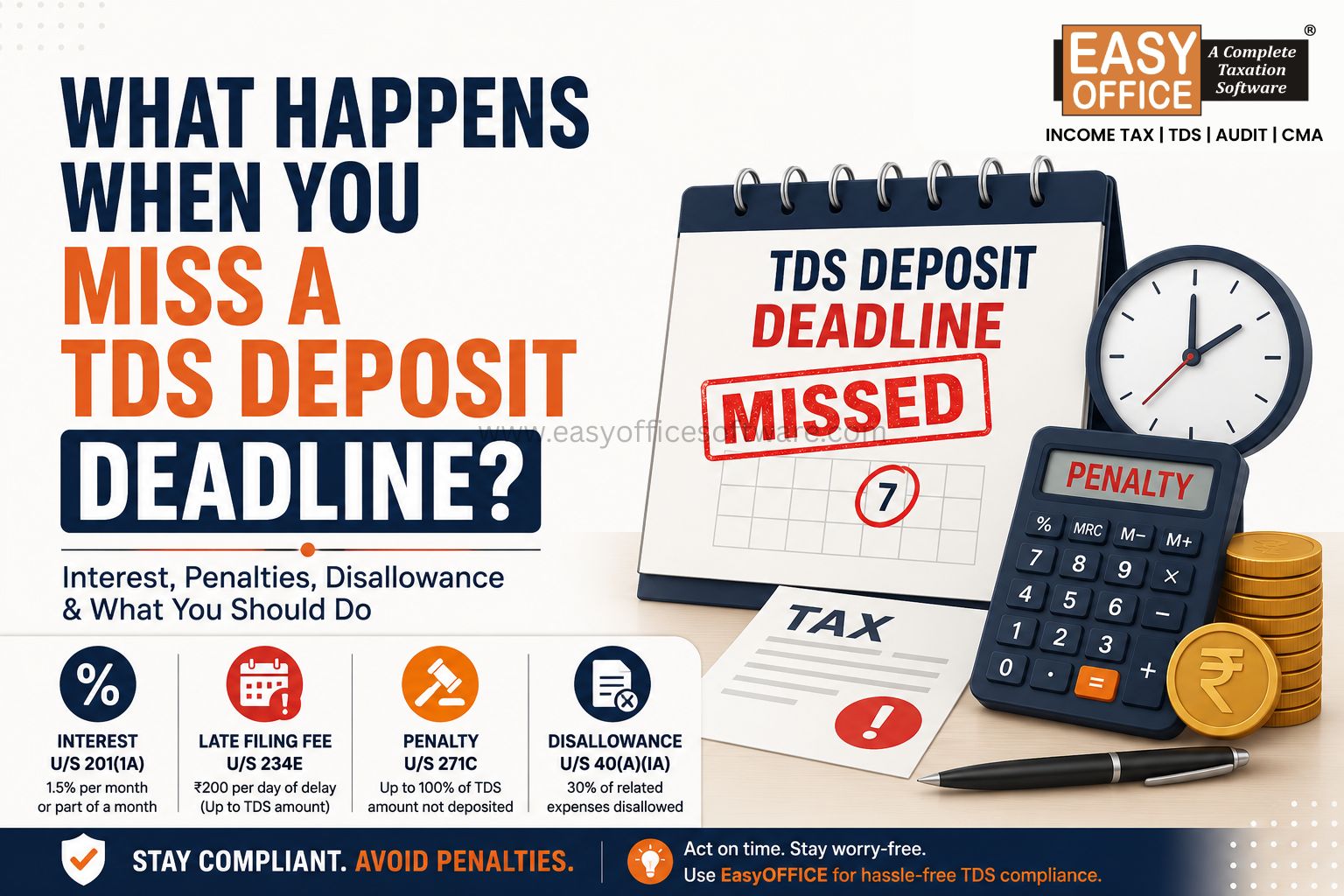

Due Dates, Penalties, and Interest

Delays in deduction, payment, or return filing may attract:

I. Interest at 1%–1.5% per month

II. Late fee of ₹200 per day

III. Penalties up to ₹1 lakh

Using the best TDS software in India ensures timely compliance and automatic deadline tracking.

Why Businesses Are Switching to Online TDS Software

Manual Excel-based TDS management is prone to errors. Modern online TDS return filing software provides:

1. Automatic rate selection

2. PAN validation

3. Challan generation

4. Return filing (24Q, 26Q, 27Q)

5. TDS certificate generation

Businesses adopting automation report up to 70% reduction in TDS-related errors.

Solutions from EasyOFFICE – Electrocom Software are designed to simplify compliance while addressing concerns related to pricing and scalability.

Frequently Asked Questions (FAQs)

Where can I get the TDS rates chart PDF for FY 2025-26?

It is advisable to rely on updated digital charts within software rather than static PDFs.

Which is the best TDS software in India?

The best solution ensures accuracy, compliance, and seamless return filing.

Is online TDS filing mandatory?

For most deductors, yes. Manual filing is no longer practical.

When is TDS deducted at a higher rate?

If the payee does not furnish PAN, TDS is deducted at 20% where no specific rate is prescribed.

Final Thoughts

TDS compliance is becoming increasingly data-driven. Referring to an updated FY 2025-26 TDS rates chart and using reliable online TDS return filing software is the most effective way to stay compliant, avoid penalties, and reduce administrative burden.

With the right technology partner such as Electrocom Software Pvt Ltd, TDS compliance becomes simple, accurate, and stress-free.

TDS rates FY 2025-26, online TDS return filing software, best TDS software in India, TDS software price, FY 2025-26 TDS rates, TDS rates chart PDF 2025-26, TDS compliance India

Related Blogs

All in one Software

- Income Tax Software

- TDS & TCS Software

- Audit e-filing Software

- CMA Data Software

Penalty for Late Filing of Income Tax Return for FY 2025-26 – Section 234F of Income Tax Act 1961

#ITR