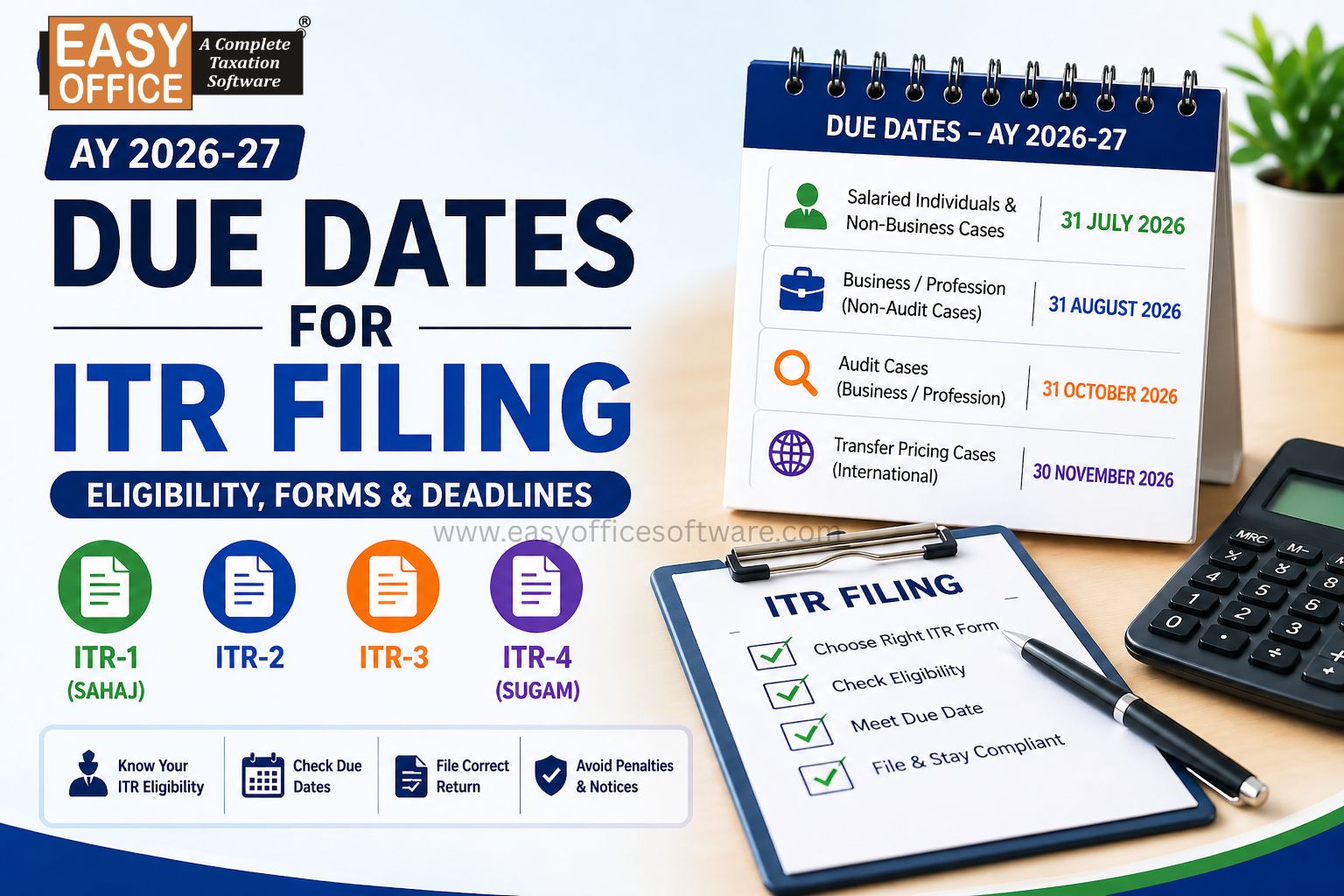

Still confused about which ITR Form is applicable to you? Separate ITR Form are filed by all type of Assessee for their source of incomes in India. This article explains applicable ITR forms for salaried individuals along with their eligibility criteria and due dates for AY 2026-27.

ITR Forms for Individuals

For Salaried Individuals, 4 ITR forms are applicable ITR-1 (SAHAJ), ITR-2, ITR-3, and ITR-4.

ITR-1 (SAHAJ)

Eligibility:

> Must be a Resident Individual

> Income should not exceed Rs. 50 Lakh

> Income Sources - Salary, Pension, up to 2 House Properties, Interest from savings accounts, FDs, Dividends, Family pension, etc.

> Agricultural Income up to Rs. 5000

> Capital Gains restricted to LTCG u/s 112A up to Rs. 125000, given that there are no past year losses carry forward (Only equity-related LTCG is allowed; other asset gains require ITR-2)

Disqualification:

- Non-Resident (NRI), Not Ordinarily Resident (NOR) individuals

- Business or professional income

- Director of any company

- Held any unlisted equity shares in the previous year

- Income from sources outside India or Foreign Assets

- Tax deducted u/s 194N (cash withdrawal)

- Tax deferred on ESOPs

- Any brought forward or carried forward losses under any income head

- Any STCG or LTCG from other assets (gold or property)

ITR-2

Eligibility:

> Individuals and HUFs

> Can be Resident (OR), Non-Ordinarily Resident (NOR), and Non-Resident (NRI)

> Director of any Company

> No upper limit on Income

> Income sources - Capital gains (STCG and LTCG), Income from more than 2 house properties, Foreign Income, Unlisted Shares

> All ITR 1 source of Income

Disqualification:

- Any Income from “Profits and Gains of Business or Profession” (PGBP) or carry forwarded Business losses

ITR-3

Eligibility:

> Individuals and HUFs with business, Partners of a Firm

> Business Owners maintaining regular books of accounts

> F&O or Intraday Traders (Mandatory Reporting of F&O turnover)

> Taxpayers who are to be Audit u/s 44AB

> Income from Virtual Digital Assets

Disqualification:

- Non-Individuals such as Companies, LLPs, or Firms

- Salary and House property income with no business connection

ITR-4 (Sugam)

Eligibility:

> Presumptive Income-

i. Residents opting for Section 44AD(Business), Turnover up to 3 Crore, (Cash Receipts are less than or equal to 5%)

ii. Residents opting for Section 44ADA (Profession), Gross Receipts up to Rs. 3 crores, (Cash Receipts are less than or equal to 5%)

iii. 44AE (Goods Carriage)

> Total Income must not exceed Rs. 50 Lakh

> Income from up to 2 House Properties

> Capital Gains restricted to LTCG u/s 112A up to Rs. 125000

Disqualification:

- Non-Resident Individual

- Insurance agents or commission earning brokers

- Speculative Income or Income from Virtual Digital Assets

- Any capital gain except LTCG u/s 112A up to Rs. 1.25 Lakh

Due Dates for ITR filing for AY 2026-27

Below are the official due dates prescribed for ITR-1, ITR-2, ITR-3, and ITR-4 for different types of taxpayers for AY 2026-27:

| Type of Taxpayer | Relevant ITR Forms | Due Date |

| Salaried Individuals & Non-Business cases | ITR-1 & ITR-2 | July 31, 2026 |

| Business/Profession (Non-Audit cases) | ITR-3 & ITR-4 | August 31, 2026 |

| Audit Cases (Business/Profession) | ITR-3 | October 31, 2026 |

| Transfer Pricing Cases (International) | ITR-3 | November 30, 2026 |

Conclusion

Choosing and filing the correct ITR form within due date ensures that the tax reporting is accurate. Using Correct ITR Form and timely filing prevent any interests, penalties, or legal notices after filing. This helps in the smooth carry forward of losses and ensures a timely refund. Tax professionals and individuals can simplify ITR selection and filing using automated income tax software.

FAQS

Q. When should I switch to ITR 2 from ITR 1?

A. When your income exceeds Rs. 50 lakh, or if you have any LTCG (> Rs. 1.25L), STCG, or more than 2 house property incomes.

Q. If I am running a small business or have income from freelancing, which ITR form should I file?

A. ITR 4 applicable if you are opting for the presumptive taxation, ITR 3 if you are a partner in a Firm or Regular Business income.

Q. Is ITR 3 mandatory if I trade in the stock market?

A. ITR 2 applicable to report capital gains in case you buy and hold shares. File ITR-3 in case of Intraday and F&O, as these are considered business income.

Q. What happens if I file the wrong ITR form?

A. In case of filing a wrong ITR form, the ITD will treat it as defective, and you will receive a notice to file a corrected return within 15 days. Failing to do so, you will have to file a belated return that may attract a late fee penalty and interest.

Related Blogs

All in one Software

- Income Tax Software

- TDS & TCS Software

- Audit e-filing Software

- CMA Data Software

Penalty for Late Filing of Income Tax Return for FY 2025-26 – Section 234F of Income Tax Act 1961

#ITR