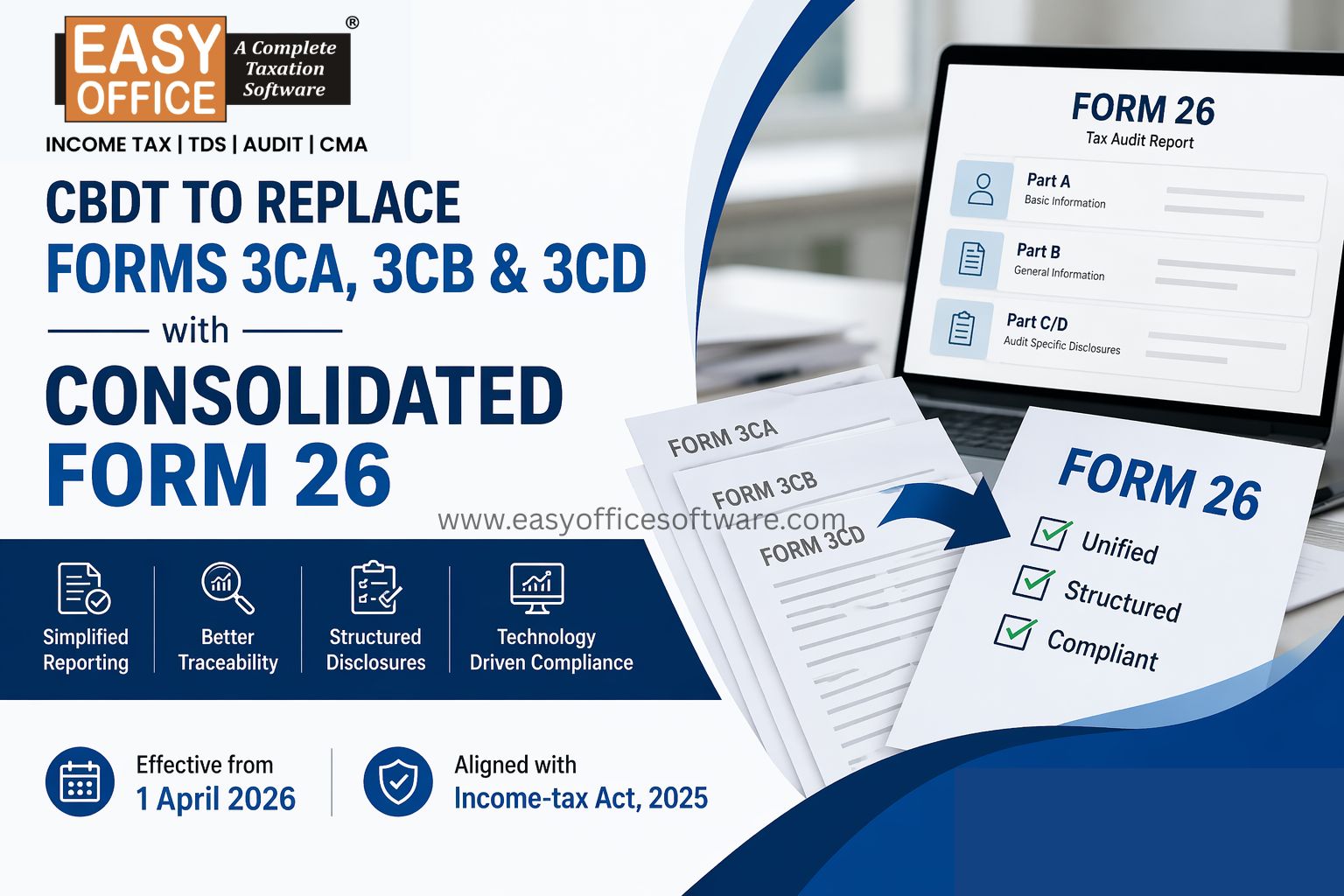

The Central Board of Direct Taxes has proposed a major structural change in tax audit reporting. The draft Income-tax Rules 2026 propose to replace Forms 3CA, 3CB, and 3CD with a single Form 26.

This move aligns with the implementation of the Income-tax Act, 2025, effective from 1 April 2026. This proposal is not merely a form replacement - it redefines how tax audit data will be captured, validated, and scrutinized under the new compliance architecture. The new system requires organizations to develop complete system capabilities that reshape the audit reporting framework for FY 2026-27 (Tax Year 2026-27) and onward.

Why CBDT is replacing Forms 3CA, 3CB, and 3CD

Under the Income-tax Act, 1961, tax audits were governed by section 44AB. Audit Reports were made in the following form:-

| Existing Form | Purpose |

|---|---|

| Form 3CA | Audit report where accounts are already audited under another law |

| Form 3CB | Audit report where accounts are not audited under another law |

| Form 3CD | Statement of particulars |

With the Income-tax Act, 2025, things have shifted. Audit rules have moved to Section 63. To match this new structure, the CBDT suggests using Form 26 as a single, all-in-one audit report. The objective is to make things simpler, keep reporting organized, and make sure disclosures line up better.

Structure of the proposed Form 26

The draft Form 26 is divided into structured parts to remove duplication and ambiguity.

Key Components of Draft Form 26

| Part | Description |

|---|---|

| Part A | Basic taxpayer particulars such as PAN, status, address, and residential status |

| Part B | General audit information, including the clause of Section 63, and business details |

| Part C / D | Audit-specific disclosures based on applicability |

The new structure creates a complete audit report system through its single document format, which replaces previous reporting formats. It eliminates the need to choose between 3CA and 3CB while retaining the detailed disclosures previously found in 3CD.

Click Here to View Form 26

Applicability of Form 26

Draft Form 26 covers two main groups:

1. Taxpayers whose accounts get audited under other laws

2. Taxpayers who cross the audit thresholds set out in Section 63 of the Income-tax Act, 2025.

Depending on the category, taxpayers only need to fill out the parts that are relevant to them. This ensures that reporting remains relevant while reducing form complexity.

Key improvements in the new audit framework

The proposed form focuses on:

i. Improved traceability of financial disclosures

ii. The organization needs to make a clear audit applicability disclosure

iii. Structured profit sharing and business activity reporting

iv. Better readiness for automated scrutiny and analytics

It reflects a shift toward data-driven compliance. The tax department uses this format to perform automated validation and reconciliation processes.

What this means for CA firms and tax professionals

Swapping out Forms 3CA, 3CB, and 3CD isn’t just a structural change. It requires process realignment. Professionals need to:

> Map old disclosures to new structured sections

> Update audit documentation workflows

> Train teams on Section 63 applicability

> Reconfigure reporting software

Manual or spreadsheet-based audit reporting may become impractical due to structured validations and cross checks embedded in the new system. That’s why reliable audit efiling software is necessary. Good tax filing software lines up your data with the right sections in Form 26, so you don’t end up with mismatches in your reports.

Additionally, your tax filing software should include audit reporting modules that integrate with Section 63. When you use audit efiling, everything just fits. You get one smooth, compliant workflow.

How technology will support the new audit regime

The Income Tax Rules, 2026 emphasize structured formats and system integration.

The new compliance model supports:

> Pre-filled data

> Centralized validation

> Reduced repetitive disclosures

> Lower interpretational disputes

The dependable audit efiling software helps companies to conduct multiple audits by decreasing their turnaround times. It ensures consistent reporting standards.

Challenges professionals must anticipate

To avoid the roadblocks, professionals must prepare for the following tasks.

> Relearn all section references.

> Update all internal templates.

> Align audit working papers.

> Manage transitional year disclosures.

The process of preparing work in advance with the trusted EasyOFFICE - audit efiling software helps professionals to avoid last-minute compliance pressure.

Conclusion

The CBDT proposal to replace Forms 3CA, 3CB, and 3CD with a unified Form 26 shows a complete transition towards organized technological methods for executing audit requirements.

For Chartered Accountants and tax professionals, Early preparation, structured workflows, and system-driven compliance will define successful audit practices under the Income-tax Act, 2025. The process of structured reporting needs dependable audit efiling software together with tax filing software that can handle new section references and updated form formats.

EasyOFFICE software for CA and tax professionals offers a unified platform to manage audits, TDS, and return filings under the new regime. The compliance tools designed for 2026-27 and future periods will keep your organization compliant with upcoming changes.

Learn more about EasyOFFICE

CBDT Updates, Tax Audit Forms, Form 3CA, Form 3CB, Form 3CD, Form 26, Income Tax Compliance, Tax Audit India

All in one Software

- Income Tax Software

- TDS & TCS Software

- Audit e-filing Software

- CMA Data Software

Penalty for Late Filing of Income Tax Return for FY 2025-26 – Section 234F of Income Tax Act 1961

#ITR